OFFERING ERP SOLUTIONS AS ONLINE SERVICES

Aki Lassila

Software Business Laboratory, Helsinki University of Technology, P.O.Box 5500, FI-02015 TKK, Espoo, Finland

Keywords: Software as a Service, business model, enterprise resource planning, value networks, online service.

Abstract: The differences between product and service business are considerable and the change of focus in a firm’s

business model from one to the other is not easy to accomplish. The objective of this paper is to study how a

software product company specialised in developing Enterprise Resource Planning (ERP) applications can

use the Software as a Service (SaaS) business model to expand its business. To software companies who

provide SaaS services, SaaS offers e.g. lowered production and distribution costs, more predictable cash

flows, and shortened sales cycle. However, in order to be able to successfully offer SaaS services the

providers have to overcome the potential risks associated with e.g. scalability, reliability, and partner

management. In this case study we concentrate on SAP and examine how the SaaS model can be

implemented by an ERP software company. Our findings include that SAP has successfully leveraged its

market leader position with its SaaS offering and expanded its customer base in the SME markets with the

help of its partner network. SAP has also been able to cope with the problems associated with SaaS and

managed to take advantage of the SaaS model’s benefits.

1 INTRODUCTION

The differences between product and service

business are considerable and the change of focus in

a firm’s business model from one to the other is not

easy to accomplish (see e.g. Hoch, D. et al. 1999,

Nambisan 2001, Cusumano 2003). For example, the

scale economies, which are associated with product

business (and especially with information goods),

are not easily achieved in service business.

Furthermore, the economies of scope (e.g. applying

domain area how-to knowledge) are harder to take

advantage of in the product business as they usually

e.g. increase the complexity of the software

development (Nambisan 2001). The Software as a

Service (SaaS) business model attempts to bridge the

gap between the software product and service

business in order for the software companies to

provide online services to their customers (SIIA

2001, Hoch, F. et al. 2001, TripleTree 2004,

Sääksjärvi et al. 2005). The SaaS model tries to

provide answers on how the software firms can at

the same time achieve the above-mentioned

economies of scale, economies of scope, and fulfil

customers’ requirements for customisation to suit

their business needs at the same time. The purpose

of this paper is to study how a software product

company can successfully adopt a more service-

oriented business model and by doing so increase

the number of its customers and access new markets

with the help of its partners.

The objective of this exploratory and descriptive

research study is to address the above-mentioned

issues and propose different ways of how they can

be solved. We use a case study, which is centred on

one particular domain area, namely Enterprise

Resource Planning (ERP), to illustrate how one

particular software company has leveraged its

domain area knowledge (which is associated with

scope economies), expanded its customer base

(enjoying from economies of scale benefits),

customised its SaaS service offering to suit its

partners’ and customers’ needs, and also leveraged

the complementary resources of its partners in

creating a packaged service offering (benefiting

from economies of aggregation). The case company

that we studied was the ERP software market leader

SAP, which has operated in the ERP (product)

business since 1972, and its SaaS offering. In this

paper we define ERP software as a firm-wide

information system that integrates key business

processes so that information can flow freely

between different parts of the firm (Laudon and

Laudon 2002), are very complex applications and

implementing them requires large investments of

money, time, and expertise (Davenport 1998). In

66

Lassila A. (2006).

OFFERING ERP SOLUTIONS AS ONLINE SERVICES.

In Proceedings of WEBIST 2006 - Second International Conference on Web Information Systems and Technologies - Society, e-Business and

e-Government / e-Learning, pages 66-73

DOI: 10.5220/0001248000660073

Copyright

c

SciTePress

addition, offering ERP software as an online service

is complicated since it requires the integration of a

range of business processes and information systems

that are vital to the customer (Ekanayaka et al. 2002,

Guah and Currie 2004). Therefore, offering ERP

software as a service is an interesting case to study.

1.1 Structure of the Paper

The paper is structured as follows. We begin by

introducing the framework that was used in this

study. Next, we review the case study’s research

methodology and in section four we present the

overview of the case company and its SaaS offering.

In section five the findings from the case study are

analysed. The final section is for discussion of the

results and also our conclusions and suggestions for

future research are presented.

2 FRAMEWORK

The framework of this study consists of the Software

as a Service business model (Cherry Tree 2000,

SIIA 2001, Hoch, F. et al. 2001, Sääksjärvi et al.

2005) and Amit and Zott’s value driver model (Amit

and Zott 2001). These models are the building

blocks that form the theoretical background of this

paper and are used as the lenses via which the case

study’s findings are analysed.

2.1 Software as a Service

The Software as a Service is a relatively new

concept although the origins of the SaaS business

model can be traced back to the time-sharing

services (Walsh 2003, Kern et al. 2002). The SaaS

model moves the focus from owning the software to

using the software as it examines the service aspect

of the software business and ways for the software

companies to offer a new value proposition to their

customers by moving away from the product-based

approach to software procurement to more service-

oriented one (SIIA 2001, Hoch, F. et al. 2001,

Ekanayaka et al. 2002, TripleTree 2004, Sääksjärvi

et al. 2005). Some of the proposed SaaS benefits for

the customers include that SaaS enables them to

focus on core competencies, offers easier access to

technical expertise, reduced implementation time,

scalability, and economic access to valuable

software applications at anytime and from anyplace

(Cherry Tree 2000, SIIA 2001, Hoch, F. et al. 2001,

Ekanayaka 2002, Kern et al. 2002, Walsh 2003). For

the SaaS providers, the proposed benefits of offering

SaaS services includes e.g. scale economies in both

production and distribution costs, expansion of the

potential customer base, more predictable cash

flows, and shortened sales cycle (Cherry Tree 2000,

SIIA 2001, Kern et al. 2002, Walsh 2003). We have

summarised the SaaS model’s benefits and risks

from the SaaS providers’ viewpoint in Table 1.

A white paper of the SIIA introduced the term

“Software as a Service” (SIIA 2001, Hoch, F. et al.

2001). SIIA’s aim was to change the perspective

from outsourcing to that of network-based services

by exploring and identifying important issues and

critical success factors for the Independent Software

Vendors (ISVs) seeking to introduce new online

services. Among the important issues that SIIA

reviewed were the new skills and resources needed

by the ISVs in order to be able to ”SaaS enable”

their existing products. This could e.g. mean

building new versions of their software products

and/or forming partnerships in order to create their

SaaS offering. SIIA (2001) and others (Cherry Tree

2000, Ekanayaka et al. 2003, Walsh 2003,

Sääksjärvi et al. 2005) have emphasized that the

ability to manage partnerships will be important

amongst the new set of skills needed by SaaS

providers because even the largest companies will

have difficulties in providing and managing all of

the components needed in creating SaaS solutions.

We propose that instead of the limited

outsourcing perspective, the SaaS business model

should be understood as a one-to-many e-commerce

arrangement dealing with digital products (see e.g.

Shapiro and Varian 1999 for a more thorough

discussion on digital products). We define SaaS as

follows: “Software as a Service is time and location

independent online access to a remotely managed

server application, that permits concurrent utilisation

of the same application installation by a large

number of independent users (customers), offers an

attractive payment logic compared to the customer

value received, and makes a continuous flow of new

and innovative software possible” (Sääksjärvi et al.

2005). SaaS services, which are also called web

services (Currie 2004), are said to be the next

generation of Application Service Provision (ASP)

services (Cherry Tree 2000, SIIA 2001, TripleTree

2004). The most important differences between the

SaaS and the “old” ASP model are that: 1) SaaS

applies an e-commerce point-of-view instead of the

ASP model's outsourcing view, 2) the SaaS model

emphasizes the capability and need to (mass)

customise customer solutions, and 3) SaaS is a

coherent business model concerned with value

creation and value appropriation whereas ASP is

more of a technical definition (Lassila 2005).

OFFERING ERP SOLUTIONS AS ONLINE SERVICES

67

More and more ISVs (not only ERP software

companies) are implementing the SaaS business

model and slowly changing their focus from

product-based business (where the customer owns

the application software and delivery infrastructure)

to providing software-based services (where the

customer “rents” the application and the SaaS

provider manages the delivery infrastructure).

However, creating a successful SaaS offering will

require more concrete models of e.g. how the issues

related to networking are managed (Gulati et al.

2000, Dyer et al. 2001), how the necessary scale

economies can be reached (performance and

scalability issues of applications need to be resolved

while meeting the customer requirements for

integration and customisation see e.g. Cherry Tree

2000, Hoch, F. et al. 2001, Susarla et al. 2003,

Walsh 2003, Guah and Currie 2004), and how the

continuous flow of product innovations i.e. novelty

for the customers (Amit and Zott 2001, Utterback

1994) could be arranged. All in all, these

observations make the SaaS model very challenging

and some of the literature has probably

underestimated the difficulties and risks (SIIA 2001,

Walsh 2003, TripleTree 2004) caused by the SaaS

model’s requirement for the firms to be able to

transform their software product business into online

service business (Nambisan 2001, Cusumano 2003,

Currie 2004, Sääksjärvi et al. 2005). However, it has

to be noted that for some ISVs the SaaS model is

more of a new sale or distribution channel and does

not mean a complete overhaul of the company's

strategy. For a software company with an existing

customer base (such as SAP), the key questions

revolve around bringing software services to market

with a minimum of disruption to current sales and

distribution channels and achieving a maximum

additive effect on sales.

2.2 Value Drivers

The value driver model of Amit and Zott enables the

evaluation of the value creation potential of different

business models through four value drivers:

efficiency, complementaries, lock-in, and novelty. In

this paper these four value drivers are used to review

and analyse the case firm and its SaaS service

offering.

Amit and Zott’s (2001) value creation model is

based on the virtual markets “in which business

transactions are conducted via open networks based

on the fixed and wireless Internet infrastructure”.

According to Amit and Zott, several characteristics

of the virtual markets, such as the ease of extending

one’s product or service range to include

complementary products, improved access to

complementary resources and capabilities, and new

forms of collaboration among firms, have an

enormous effect on how value can be created. Value

creation opportunities in virtual markets may arise

e.g. from new ways to combine information goods,

physical products and services, and integration of

resources and capabilities among partners.

Furthermore, the network-based value perspective of

Amit and Zott’s model provides a good background

to explore and explain the driving forces behind the

SaaS providers’ reasons for partnering and the

factors that affect these partnerships.

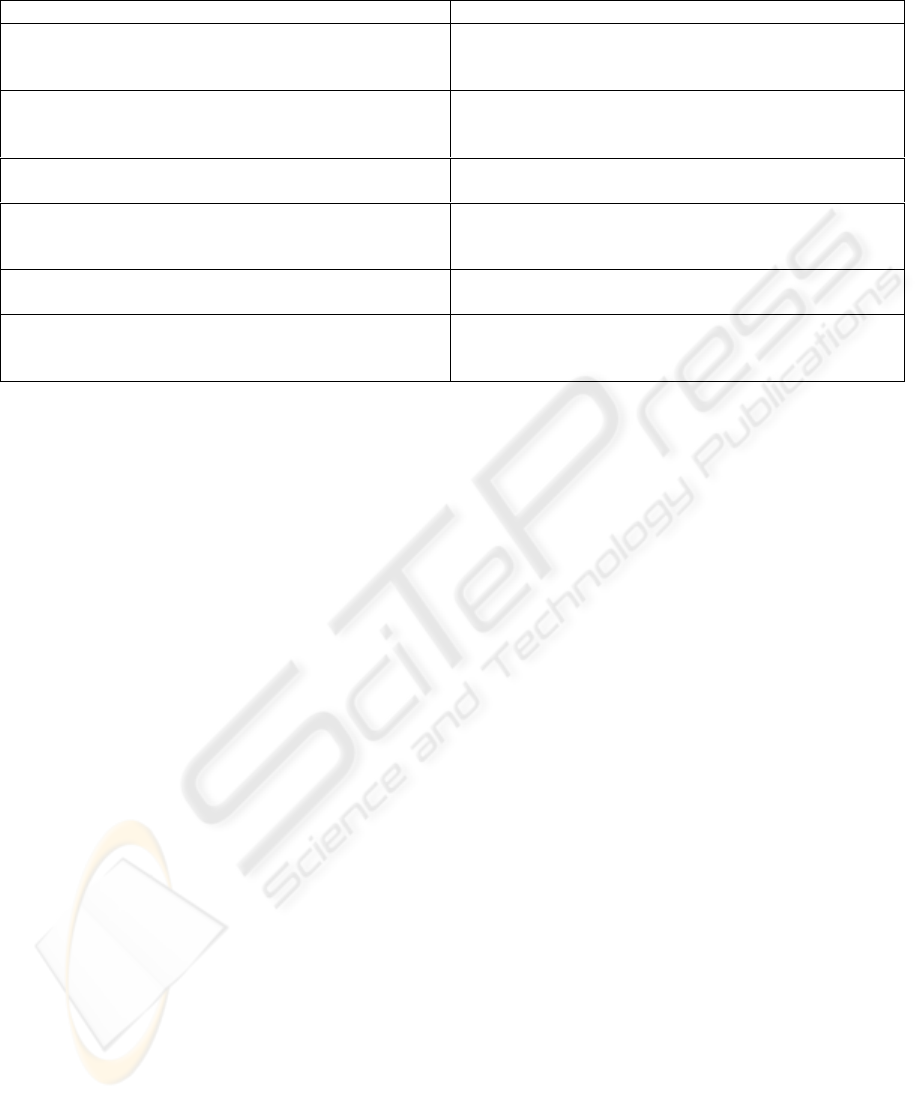

Table 1: The benefits and risks of the SaaS model for the provider (Sääksjärvi et al. 2005).

Benefits for the SaaS provider Risks for the SaaS provider

1. SaaS enables economies of scale in production

and distribution (one-to many offering)

1. It is difficult to manage the complex network of

suppliers, which is required for integrating the

product and service businesses

2. The cash flows from SaaS are more predictable

than in traditional software sales (recurring revenue)

2. Moving to the SaaS model initially reduces the

turnover as the revenue comes from service fees

instead of license sales

3. SaaS expands the potential customer base 3. Performance and scalability issues are to be

expected, depending on the technical solution used

4. The sales cycle of SaaS services is shorter than

that of traditional software sales

4. High initial investment in starting the SaaS

business (building and maintaining the required IT

infrastructure and costs of buying 3rd party software)

5. SaaS lowers version management and

maintenance costs

5. The customisation of the SaaS applications

typically incurs extra costs

6. By successfully integrating products and

services into a SaaS offering, provider creates

barriers to entry for competitors

6. Requires commitment to a more frequent

release/upgrade cycle

WEBIST 2006 - SOCIETY, E-BUSINESS AND E-GOVERNMENT

68

The value creation model is based on the value

chain framework (Porter 1985), the theory of

creative destruction (Schumpeter 1942), the

resource-based view (Barney 1991), strategic

network theory (e.g. Dyer and Singh 1998, Gulati et

al. 2000) and transaction cost economics

(Williamson 1975). Amit and Zott (2001) emphasize

the distinction between a business model and a

revenue model: the business model primarily refers

to value creation whereas the revenue model is

centred on value appropriation. By the term “value”

Amit and Zott refer to the total value created for all

parties involved in the network that the firm’s

business model compasses. The four value drivers

help in assessing the total value that can be

appropriated by the participants of a particular firm’s

business model i.e. in this case SAP and its

partners/complementors, and their customers.

In Amit and Zott’s model the most important

value driver is efficiency. Efficiency enhancements

include e.g. reduction of transaction costs,

achievement of scale and scope economies,

reduction of search costs etc. Another source of

value creation are complementaries, which are

present whenever having a bundle of goods together

provides more value than the total value of having

each of the goods separately (for a more thorough

discussion on bundling and economies of

aggregation see e.g. Bakos and Brynjolfsson 1999).

Business models can also create value by

capitalising on complementaries among activities

e.g. when firms co-operate and create a SaaS

offering together. The virtual markets open new

value creation possibilities since new relational

capabilities, skills, and assets (i.e. shared resources)

between firms can be exploited e.g. between online

and offline capabilities in order to create sustainable

advantage.

According to Amit and Zott (2001), the value-

creating potential of a business model depends also

on the extent of which it is able to engage customers

to repeat transactions and this value driver is called

the lock-in. Lock-in usually refers to the switching

costs faced by clients who consider alternative

services or products from other firms. Lock-in

includes e.g. customer loyalty programs,

customisation, and branding. The fourth value

driver, novelty, consists of new ways of conducting

transactions, new product or service innovations, or

new ways of combining products and services (as in

the case of the SaaS business model). Usually the

four value drivers and their effects are interrelated

with one another.

3 CASE STUDY

This exploratory research study follows the

interpretive approach to qualitative research as we

conduct a case study and analyse the findings using

Klein and Myers’s proposed set of principles (Klein

and Myers 1999) in conducting our research.

The case study’s unit of analysis is the SAP’s

SaaS business model, which we think provides

useful insights for other software companies on how

to create a successful SaaS offering. In this case

study we wish to explore 1) how a company with an

existing customer base can start offering SaaS

services, 2) expand its customers base with the help

of its partners, 3) overcome the problems associated

with SaaS, and 4) take advantage of the benefits of

the SaaS business model. Our propositions were

reviewed earlier in section two were the framework

was presented. The earlier presented framework is

used as the criteria with which the case study’s

findings are analysed.

For this case study information was gathered via

interviews and discussions with SAP’s employees

and partners. In addition, information was also

gathered from newspapers and trade journals, web-

based news services, and from the company’s own

communication materials such as annual and

quarterly reports, press releases, product

descriptions, and own web pages.

4 SAP AND ITS SAAS OFFERING

SAP was founded in 1972 and its headquarters are in

Walldorf, Germany. SAP has operations in more

than 50 countries and the company is listed on

several stock exchanges, including the Frankfurt

stock exchange and NYSE. In, SAP established a

specialised subsidiary called SAP Hosting, which

specialises in operating and managing SAP solutions

in order to be “a flexible hosting provider and ASP

for SAP” (SAP 2000). Currently SAP Hosting

operates over 300 SAP systems for their customers,

employs around 375 staff, and supports more than

130,000 users in four data centres in Germany and

the United States (SAP 2005a). SAP Hosting’s

customer base ranges from “midsize firms right

through to the TOP 500 companies in the world”

(SAP 2005a). For reference, SAP Group’s and SAP

Hosting’s essential financial figures are shown in

Table 2. The figures in Table 2. should be read with

caution since they are somewhat misleading because

SAP has stated in its annual reports that “portion of

SAP’s external hosting revenue is not included here

but in the revenue numbers of the subsidiaries,

which sell the services to the customers of SAP”.

OFFERING ERP SOLUTIONS AS ONLINE SERVICES

69

This means that part of SAP’s SaaS revenues are

reported in the SAP Group’s product and service

revenues and do not show up in the SAP Hosting’s

financials. Furthermore, IDC estimated that in 2003,

SAP’s SaaS revenue was 53.4 million dollars (note

that it was twice the figure that SAP Hosting

reported) representing 24 per cent growth from

2002, which placed SAP the eight largest amongst

the worldwide Top 10 SaaS providers (e.g.

Salesforce.com and Oracle being fourth and fifth

respectively, Mizoras 2004). This being the case, it

is not possible to draw very accurate conclusions

from these financial figures although it is certain that

the SaaS services still represent only a very small

portion of the whole SAP Group’s revenues.

However, from these figures we can see the trend

that SAP’s SaaS business has grown faster than

either total, product, or service revenues and that

business has been profitable with the exception of

2002, which was financially a bad year for the whole

SAP Group.

4.1 Offering ERP Software as a

Service

From 2000 onwards, SAP has offered its mySAP

ERP software as a service via SAP Hosting and via

its SaaS partner and reseller network. Following the

SAP Group’s market segmentation strategy, the SAP

Hosting targets its SaaS offering towards the

medium-sized and large, Top 500 companies in

order to avoid or lessen the channel conflict with its

SaaS partners. SAP’s SaaS partners include ACS,

Corio, CSC, and USInternetworking. In Figure 1. we

present an overview of the SAP’s SaaS business

model.

Figure 1: SAP's SaaS business model.

In order to create its own mySAP SaaS offering,

SAP uses e.g. HP as its IT infrastructure provider.

The SAP’s SaaS offering consists of the mySAP

Business Suite, which includes Enterprise Resource

Planning (ERP), Customer Relationship

Management (CRM), Product Lifecycle

Management, Supplier Relationship Management

(SRM), and Supply Chain Management (SCM)

applications. These are further divided into

functional modules, which include e.g. Sales &

Distribution (SD), Material Management (MM),

ERP Financials, and ERP HR. From these modules

the customers can select the services they want to

purchase. It is also possible for the customers to

provide and maintain some of the mySAP

functionality by themselves and buy only some parts

of their ERP solution as a SaaS service from the

SAP or SAP’s SaaS partners.

For a relatively small monthly subscription fee

(compared to the high ERP product license and

Table 2: SAP Group’s and SAP Hosting’s financial figures 2000-05 (source: SAP’s annual reports).

2000 2001 2002 2003 2004

SAP Group (in millions of €)

Total revenue 6,264 7,341 7,413 7,024 7,515

Rev. increase % 23% 17% 1% -5% 7%

Product revenue 2,459 2,581 2,291 2,148 2,361

Prod. increase % 27% 5% -11% -6% 10%

Service revenue 2,045 2,549 2,618 2,252 2,273

Serv. increase % 5% 25% 3% -14% 1%

Net income 616 581 509 1,077 1,311

Return on sales 16% 15% 15% 25% 28%

Employees 24,177 28,410 28,797 29,610 32,205

SAP Hosting (in thousands of €)

Revenue 6,038 12,702 15,410 27,611 45,696

Rev. increase - 110.3% 21.3% 79.2% 65.5%

Net income 531 1,192 -4,705 409 3,766

Return on sales 8.8% 9.4% -30.5% 1,5% 8.2%

Employees 54 71 115 113 220

WEBIST 2006 - SOCIETY, E-BUSINESS AND E-GOVERNMENT

70

implementation costs), the SaaS customers can

subscribe to these mySAP SaaS services. The

customer fee is usually per customer (end user) per

month based subscription fee, which depends on the

amount of functionality and customisation of the

SaaS service. The SAP’s SaaS revenue model is

straightforward: SAP Hosting receives recurring

revenue from its own customers and SaaS partners

pay either the mySAP software license fee (which

depends on the chosen functionality and modules) or

the partner and SAP sign a revenue sharing

arrangement.

It has to be also noted that the SAP’s SaaS

partners usually do not offer the whole range of the

Business Suite’s functionality, instead they are

usually concentrating on offering only some of the

modules of the Suite to suit a certain customer

segment’s needs. In addition, the SAP’s partners

usually offer also other companies’ software as a

service and integration and customisation services

for these as well. The complexity of the ERP

software makes offering it as a service difficult. The

number of possible combinations of functionality

and features the SaaS customers can choose, what

their ERP SaaS service consists of, and how it is

implemented is very high. That is why SAP and its

SaaS partners also offer consultation services. These

consultation services usually include design and

planning, integration, customisation,

implementation, and training services in order to

create and offer the customer an ERP solution that

suits their needs. Implementing an ERP solution can

be an extremely complex task especially if the

amount of functionality is high and customer’s

customisation requirements are numerous. This

makes ERP software’s suitability for SaaS services a

very challenging task: how to productise the service

offering and reach economies of scale while still

fulfilling the customers’ customisation

requirements? Usually this problem is handled by

the SaaS providers by limiting the number of

mySAP modules they offer and by offering only

limited customisation features. Naturally the

complexity also affects the implementation time

since a plain vanilla ERP solution with very little

customisation can be more quickly be put in use by

the SaaS customer and it also costs less.

Unfortunately, these plain vanilla solutions often do

not suit the customer’s needs and requirements

regarding e.g. integration.

5 CASE STUDY’S FINDINGS

For SAP, the SaaS business model has been

successful: SAP has been able to increase its sales,

international operations, and customer base

profitably without having to make huge investments

e.g. in different countries’ sales and support

personnel. The case study’s findings in light of the

value creation model are summarised in Table 3.

Furthermore, SAP has been able to capture all of

the previously listed benefits of the SaaS business

model (see Table 1.) except for the item number six

because SAP especially wants other companies to

also offer mySAP-based SaaS services. This is part

of SAP’s overall strategy of growing its partners,

complementors, and resellers business as well as its

own at the same time. As the market leader, SAP has

over 50 per cent share of the overall ERP software

market and it has chosen the growth strategy of

growing with its partners (see e.g. Hoch, D. et al.

1999 and Gawer and Cusumano 2002).

SAP has also taken advantage of its domain area

how-to knowledge and succeeded in offering its

mySAP Business Suite as a service to a wider

customer base through its SaaS partners and

resellers. In essence, SAP has managed to reach

economies of scale while taking advantage of

economies of scope i.e. its ERP software can now be

offered to and used by a larger number of customer

companies. This has been made possible by SAP,

which has successfully combined its own product-

based business with its partners’ service business

related skills and assets. By enabling its partners to

sell mySAP SaaS services, SAP has also lowered its

costs associated with sales, distribution,

customisation, and customer support (SAP’s

partners handle them) and also started receiving

recurring revenue.

In addition, the risks associated with the SaaS

model have also been successfully dealt with. SAP

has downplayed the possible channel conflicts and

selected partners (such as HP as its IT infrastructure

provider) that complement its own skills, resources,

and e.g. geographical coverage. Also, the underlying

technology of mySAP software makes it a scalable,

web-enabled application and therefore suitable for

online services. Furthermore, instead of (initially)

reducing revenue due to the adoption of the SaaS

model, SAP has increased its software license sales

through its partners and expanded its potential

customer base successfully to the SMEs, which are a

lucrative market for the big ERP software

companies.

To summarise, even though offering ERP

software as a service is a complex matter SAP has

successfully taken advantage of the SaaS business

model’s benefits and has managed to downplay the

associated risks. Also the SAP’s SaaS partners and

resellers have benefited from their complementary

skills and assets in creating a bundled service

offering.

OFFERING ERP SOLUTIONS AS ONLINE SERVICES

71

Although this case study concentrated on only

one company and its SaaS offering, the results of

this case study can be said to be generalisable on the

analytical level (level-1 inference), which is

commonplace with case studies (Yin 2003).

According to Lee and Baskerville’s generalisability

framework, this research study’s findings would fall

into the category of generalising from data to

description (Lee and Baskerville 2003).

6 DISCUSSION AND

CONCLUSIONS

The purpose of this paper was to study how a

software product company can use the Software as a

Service model to expand its business. We conducted

a case study of SAP and its SaaS offering and found

out that by successfully managing to solve or avoid

the associated risks and by taking advantage of the

SaaS model’s benefits SAP managed to increase its

sales, potential customer base, and started receiving

recurring revenue. Furthermore, also SAP’s SaaS

partners have benefited from the usage of the SaaS

model. However, it needs to be said that for SAP, its

SaaS service offering is more of an additional sale

and distribution channel and does not represent a

major renewal of the company's strategy.

On the basis of this study, we can say that the

SaaS business model can be a very successful part of

a large software firm’s strategy, especially when its

primary markets are saturated (the very large, top

500 companies already have ERP systems in place).

In addition, on the basis of our analysis we think that

instead of just concentrating on efficiency

improvements, the sustainable way to generate value

using the SaaS model is to provide easy and low-

cost access to useful software applications, based on

a broader set of value sources i.e. complementaries,

novelty, and lock-in.

In conclusion, since this study concentrated only

on exploring the SAP’s and its partners’ SaaS

offerings, the generalisability and transferability of

our findings are limited. Therefore, further studies

should be conducted in order to study SAP‘s SaaS

customers, SAP’s SaaS partners, and also different

vertical segments where ERP software is used in

order to gather a more comprehensive view on the

SaaS ecosystem that has evolved around the

platform leader SAP. Also, in order to gain more

extensive and detailed understanding of the SaaS

business model and its implications to the software

companies in general, also other software companies

and their SaaS offerings, preferably in different

application domain areas, should be investigated.

REFERENCES

Amit, R. and Zott, C., 2001. Value Creation in E-business.

Strategic Management Journal, 22(6/7), 493-520.

Bakos, Y. and Brynjolfsson, E., 1999. Bundling

Information Goods: Pricing, Profits, and Efficiency.

Management Science, 45(12), 1613-1630.

Table 3: Sources of value creation in SAP’s SaaS offering.

Efficiency Complementaries Lock-in Novelty

1. Scale economies: lower

distribution and marketing

costs of SW, lower

customer support and

billing costs

1. Bundling offers

economies of aggregation:

enables brand leveraging of

the SAP and local, domain-

area knowledge of partners

1. Co-branded, tailored

ERP offering to suit both

the SaaS partners’ and

SaaS customers’ needs and

requirements

1. ERP as a service offering

via SAP’s own and

partners’ sales and delivery

channels

2. Scope economies: SAP

provides ERP

implementation how-to

knowledge to a larger

audience

2. One-stop shopping: ERP

software and

implementation plus

hosting and maintenance.

2. High-volume repeat

transactions: recurring

revenue from joint ventures

and SaaS partners’

customers

2. SMEs are now able to

select an affordable mySAP

ERP service to suit their

needs

3. Provides an easy, low

cost, and low risk access to

new markets of SMEs

3. Reduced search

(efficiency related

offering): SAP’s partners

act as the sales and

distribution channel

3. Efficiency features and

complementary service

offering both attracts and

retains customers

4. SAP and its partners can

focus on their own core

competencies

4. SAP benefits from its

ERP software market

leader’s advantage and

positive feedback effects

WEBIST 2006 - SOCIETY, E-BUSINESS AND E-GOVERNMENT

72

Barney, J., 1991. Firm Resources and Sustained

Competitive Advantage. Journal of Management,

17(1), 99-120.

Cherry Tree, 2000. Second Generation ASPs. Spotlight

Report, Cherry Tree & Co., Retrieved August 30,

2005, from http://www.triple-

tree.com/research/technology/asp_sep_01.pdf

Currie, W., 2004. The Organizing Vision of Application

Service Provision: A Process Oriented Analysis.

Information and Organization, 14, 237-267.

Cusumano, M., 2003. Finding Your Balance in the

Products and Service Debate. Communications of the

ACM, 46(3), 15-17.

Davenport, T., 1998. Putting the Enterprise into the

Enterprise System. Harvard Business Review, July

1998, 121-131.

Dyer, J. and Singh, H., 1998. The Relational View

Cooperative Strategy and Sources of

Interorganizational Competitive Advantage. Academy

of Management Review, 23(4), 660-679.

Dyer, J., Kale, P. and Singh, H., 2001. How to Make

Strategic Alliances Work. Sloan Management Review,

Summer 2003, 37-43.

Ekanayaka, Y., Currie, W. and Seltsikas, P., 2002.

Delivering Enterprise Resource Planning Systems

through Application Service Providers. Logistics

Information Management, 15(3), 192-203.

Ekanayaka, Y., Currie, W. and Seltsikas, P., 2003.

Evaluating Application Service Providers.

Benchmarking, 10(4), 343-354.

Gawer, A. and Cusumano M., 2002. Platform Leadership,

Harvard Business School Press, Boston, MA.

Guah, M. and Currie, W., 2004. From ASP to Web

Services: Identifying Key Performance Areas and

Indicators for Healthcare. In Proceedings of the 12th

ECIS. Retrieved August 30, 2005, from

http://is.lse.ac.uk/asp/aspecis/

Gulati, R., Nohria, N. and Zaheer, A., 2000. Strategic

Networks. Strategic Management Journal, 21, 203-

215.

Hoch, D. et al., 2000. Secrets of Software Success,

Harvard Business School Press, Boston, MA.

Hoch, F. et al., 2001. Software as a Service: “A to Z” for

ISVs, Software & Information Industry Association

(SIIA). Washington, DC, Retrieved August 30, 2005,

from http://www.siia.net/estore/pubs/SAZ-01.pdf

Kern, T., Kreijger, J. and Willcocks, L., 2002. Exploring

ASP as Sourcing Strategy: Theoretical Perspectives,

Propositions for Practice. Journal of Strategic

Information Systems, 11, 153-177.

Klein, H. and Myers, M., 1999. A Set of Principles for

Conducting and Evaluating Interpretive Field Studies

in Information Systems. MIS Quarterly, 23(1), 67-94.

Lassila, A., 2005. Moving from Product-Based Business

to Online Service Business. In Proceedings of the

IADIS e-Commerce Conference, 109-117.

Laudon, K. and Laudon J., 2002. Management

Information Systems: Managing the Digital Firm,

Prentice Hall, Upper Saddle River, NJ.

Lee, A. and Baskerville, R., 2003. Generalizing

Generalizability in Information Systems Research.

Information Systems Research, 14(3), 221-243.

Mizoras, A., 2004. Worldwide Software as a Service 2003

Vendor Shares: SaaS and Enterprise ASP Competitive

Analysis. IDC Competitive Analysis, IDC #32055.

IDC, 2004. U.S. Software as a Service 2004-2008 Forecast

by Delivery Model. IDC - Industry Developments and

Models, IDC # 31267.

Nambisan, S., 2001. Why Service Business are not

Product Businesses. MIT Sloan Management Review,

42(4), 72-81.

Porter, M., 1985. Competitive Advantage: Creating and

Sustaining Superior Performance, Free Press, New

York, NY.

SAP, 2000, SAP Annual Report 2000. Retrieved August

30, 2005, from http://www.sap.com

SAP, 2005a, SAP Hosting: Company Portrait. Retrieved

August 30, 2005, from http://www.saphosting.com

SAP, 2005b, SAP Annual Report 2004, Retrieved August

30, 2005, from http://www.sap.com

Schumpeter, J., 1942. Capitalism, Socialism and

Democracy. Harper, New York, NY.

Shapiro, C. and Varian, H., 1999. Information Rules: a

Strategic Guide to the Network Economy, Harvard

Business School Press, Boston, MA.

SIIA, 2001. Software as a Service: Strategic

Backgrounder. Software & Information Industry

Association (SIIA), Washington, D.C. Retrieved

January 13, 2004, from www.siia.net

Susarla, A., Barua, A. and Whinston, A., 2003.

Understanding the Service Component of Application

Service Provision: An Empirical Analysis of

Satisfaction with ASP Services. MIS Quarterly, 27(1),

91-123.

Sääksjärvi, M. and Lassila, A.,2005. Role of The

Customer Value in the Software as a Service Concept:

Empirical Evaluation of the Factors Affecting the

Customer Lock-In of the Online Newspapers. In

Proceedings of the 5th IFIP I3E Conference, 543-557.

TripleTree, 2004. Software as a Service: Changing the

Paradigm in the Software Industry. SIIA and

TripleTree Industry Analysis Series. Washington, DC.

Retrieved August 30, 2005, from http://www.triple-

tree.com/research/technology/saas_aug04.pdf

Utterback, J., 1994. Mastering the Dynamics of

Innovation, Harvard Business School Press, Boston,

MA.

Walsh, K., 2003. Analyzing the Application ASP Concept:

Technologies, Economies, and Strategies.

Communications of the ACM, 46(8), 103-107.

Williamson, O., 1975. Markets and Hierarchies, Analysis

and Antitrust Implications: A Study in the Economics

of International Organization, Free Press, New York,

NY.

Yin, R., 2003. Case Study Research: Design and Methods

,

Sage Publications, Thousand Oaks, CA.

OFFERING ERP SOLUTIONS AS ONLINE SERVICES

73