Green Innovation within Materials Flow Cost: Opportunities and

Challenges

Karrar Abdulellah Azeez

University of Kufa, Faculty of Administration and Economics, Department of Accounting, Najaf, Iraq

Keywords: Material Flow Cost Accounting, Green Innovation, Opportunities, Challenges.

Abstract: The paper tries to identify the opportunities and challenges of material flow cost accounting via the green

innovation, the green innovation is crucial for the development of manufacturing operations as it supports

the basic needs of the costumers including production, suppliers, workers. Lighting the problem of

traditional cost systems that unable to provide sufficient data for management include waste and loss during

production processes for focusing on the value of raw materials, energy and water generated during

production processes .Thus reflected on the lack of production efficiency and lower product quality. The

analytical quantitative approach was adopted to employ the material and energy flow cost accounting

technique to identify opportunities for improvement in the production process of the produced green cement.

The research reached several conclusions, the most important of which are sing the material flow cost

accounting technique and green innovation, the variable costs decreased and at the same time the production

efficiency increased by achieving less inputs than the outputs, as well as achieving technological change by

changing the type of fuel in the furnaces.

1 INTRODUCTION

Recently, interest in environmental issues and their

problems has increased clearly, as a result of many

motives and pressures, including the shortage of

available resources and energy and the high rates of

environmental pollution, which caused many

economic problems, including the high costs

resulting from waste and loss of raw materials and

energy resources, and the decrease in the

productivity of natural systems due to Pollution, and

the emergence of costs necessary to address

environmental impacts, which necessitated the need

to assist the administration in developing appropriate

solutions to solve these problems(Baumer-Cardoso

et al., 2020; Huang et al., 2019; Syarif & Novita,

2019). By resorting to material flow cost accounting,

we can obtain a clear detail about the flow of

materials at each stage of production and determine

the amount of material and energy losses and their

locations, and thus this data has an important role in

assisting managers in making decisions that help in

managing costs and reducing them appropriately to

reach to better competitive levels(Huang et al.,

2016). It also works to determine the flows of

materials and energy through the value creation

system during a certain period of time and evaluate

the potential of cleaner production at the unit level

and the initial estimate of the costs of waste

generation(Wahyuni, 2009) . The main idea of

material flow cost accounting is based on tracking

material flows and energy use and is measured in

terms of quantitative and financial units(ISO14051,

2011). Waste is seen as a type of product whose cost

must be calculated, as is the case with good

products, which helps economic units to determine

the value that cannot be obtained as a result of

wastage(Kokubu & Nakajima, 2004).

Green innovation can be described as improving

productivity by economic units and making their

production green, which contributes to continuous

improvement and helps protect the environment and

achieve sustainability(Abdullah et al., 2016). The

green product is a green strategy that focuses on the

impact of production on the environment, and

emphasizes the elimination of environmental waste

related to the unnecessary use of water, energy and

greenhouse effects, without affecting the costs and

costs of the product with the aim of protecting the

environment and society(Farias et al., 2019).

Innovation is a product that uses environmentally

friendly materials that can self-degrade while

Azeez, K.

Green Innovation within Materials Flow Cost: Opportunities and Challenges.

DOI: 10.5220/0010828400003168

In Proceedings of the 1st International Conference on Finance, Information Technology and Management (ICFITM 2021), pages 23-27

ISBN: 978-989-758-576-0

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

23

following their life cycle stages to ensure that they

remain within an environmental commitment, which

includes no use of harmful substances, use of

minimal materials and energy, and recyclable

packaging(Baumer-Cardoso et al., 2020). The

benefit of green innovation emerges through

attention to reducing pollution, improving resource

productivity, increasing the efficiency of energy and

materials use, improving environmental

performance, as well as reducing the costs of

produced materials(Huang et al., 2016). Green

innovation also contributes to the conservation of

resources by recycling them and that the resources

have a lower environmental impact at all stages of

the product life cycle(Biswas & Roy, 2016).

The green innovation is one of technologies that

are involved in energy saving, pollution prevention,

waste recycling, and green product design , which

uses environmentally friendly materials that can

self-degrade. The traditional cost systems cannot

provide sufficient data for management related to

waste and loss during the operational activities and

unable to show the value of raw materials, energy

and water. The key to move from opportunities of

integrating a green innovation with materials flow

cost for improvement production process by

generate a green products, trying to reduce the

environmental emissions, and optimal using of

resources.

Green innovation contributes significant benefits

to the environmental performance and competitive

advantage. This paper argues to show the

opportunities of integrating green innovation with

materials flow cost are for improving the production

process by providing green products, trying to

reduce the environmental emissions, and optimal

using of resources. the application of material flow

cost in light of green innovation has important for

industry,considering that manufactural companies

still depend on traditional methods of production,

which cause dangerous wastes on the environment.

By monitoring production since the entry of raw

materials to the stage of obtaining the ready-to-use

product, the green product for the purpose of

enhancing the competitiveness of the company. As

well as trying to control waste of materials through

the method of internal recycling of factors. The

paper has divided three sections, introduction is first

one. The second section is materials and methods.

Conclusions is last section.

2 MATERIALS AND METHODS

2.1 The Sample

The paper has conducted in the national company of

cement industry, and data on 2020 used to conduct

the results .

2.2 The Procedures

Four procedures have been taken to develop

materials flow cost accounting through the green

innovation. The stages of cement industry (raw

materials mills, rotary kilns, cement mills, and

packaging), these will classify based on

methodology of materials flow cost accounting

using procedures (Plan-Do- Check-Act)(ISO14051,

2011) as follows:

Plan: the first process includes several acts that

clarified according to(Kokubu & Nakajima, 2004;

Syarif & Novita, 2019): identify the required

expertise , the expertise of engineers and workers in

the production department and in the management

and control of production planning, in order to

collect data on the production quantities needed for

analysis.

Do: the second step has several procedures that can

be clarified according to(Syarif & Novita, 2019;

Sygulla et al., 2014): Quantitative measurement of

flows: The inputs and outputs of each center has

measured, the resources received from a previous

job center, and the outputs are the two items good

and spoilage produced units.

Check: according of this step(Dekamin & Barmaki,

2019) Summarizing the data and analyzing the

results: preparing a scheme that combines the costs

of good and wasted product in operations called "

Cost Flow Matrix". The results are according to the

material flow cost accounting, which calculated the

total manufacturing costs amounted to

(50715031643) dinars, and these costs are

distributed between the good product and the

defective or lost product, where the costs of each of

the costs of the good product = 22438916428 dinars,

and the costs of the defective or lost product =

28276115215 dinars.

Act: This is an important step because it has impact

on the all activity of company as a result of

transparency in the flows of materials and

energy(Kokubu & Nakajima, 2004). The results is

ICFITM 2021 - INTERNATIONAL CONFERENCE ON FINANCE, INFORMATION TECHNOLOGY AND MANAGEMENT

24

improve financial and environmental performance

which identified and evaluated before starting a

cycle again. Moreover, replacing better quality

materials, improving processes, modifying

production lines or products, and development

activities related to material and energy efficiency.

For supporting cost-benefit analysis of the proposed

methods in the cement industry that consumes a lot

of natural resources, electric power, fuel and water.

In this paper, cement industry can create a new item

called “Green Cement” from the process of internal

recycling of all cement kiln dust, which is collected

from the air leaving the rotary kilns by depositing it

by electrostatic dust precipitators to the stage of

cement mills, and from here it can be We consider

this product to be environmentally friendly and for

the laboratory at the same time, as it will achieve

financial savings for the laboratory (the study

sample) by converting the production pattern from

resistant cement to the production of green cement,

showed in tables(1 and 2).

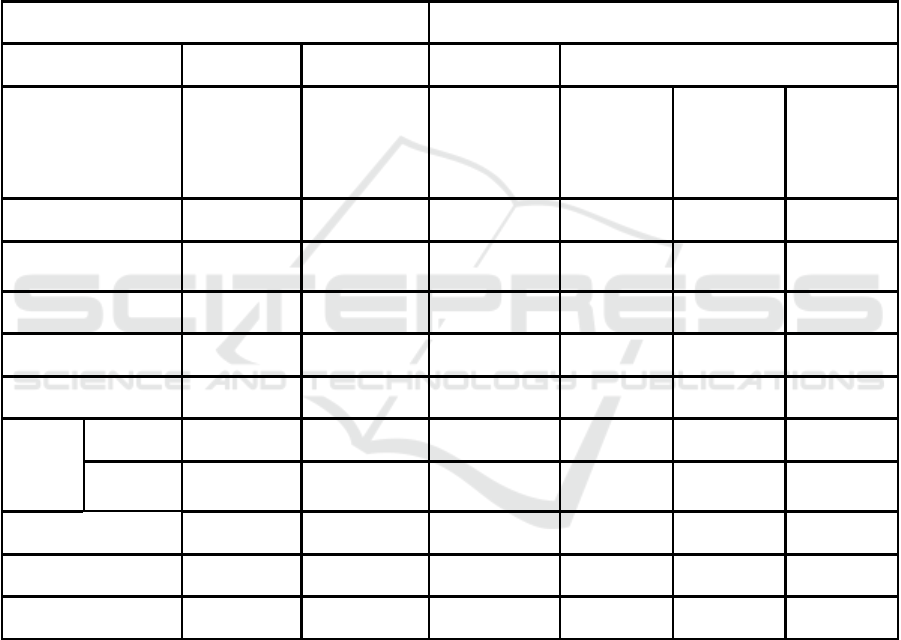

Table 1: The flow cost of job centers.

Input Output

MFCA elements Quantity cost bagged cement wastage losses

(Ton) (Dinar)

product

477474 (Ton)

final cement

wasted 7447

ton

27574 bags

waste

d

Recycled

cement

90110Ton

Power final

cement

first stock 9154 15055444 - - - -

Quantity of cement

receive

d

700795 99997951949 99705495914 1579995099 - -

new material (bag) 1577450 9195094144 9141119444 - 5590144 -

other stock 145 15055444 - - - -

User of material - 91459901049 - - - -

Power

Electricity 9901901 0191111 5515119 - 1104 9599971

Oils and

greases

995145 19947971 19947971 - - -

system - 5145175509 5911049411 50955794 79595015 -

waste management - 195159 - 195159 - -

Total 59195995777 99051199091 1041151999 77151955 9599971

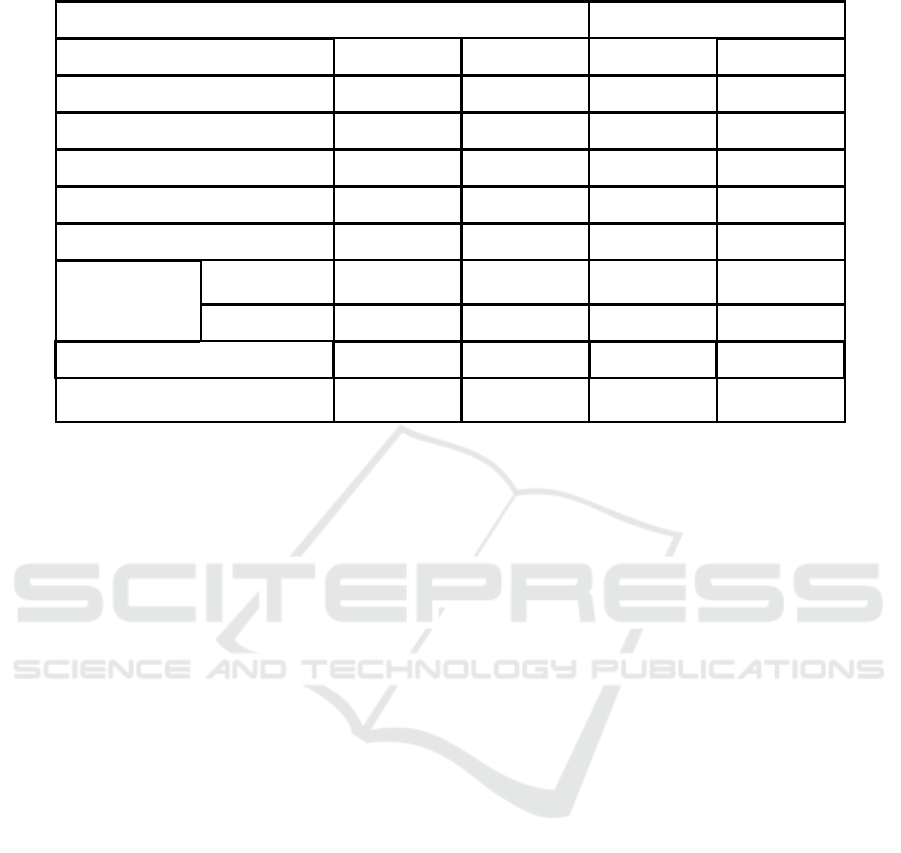

Table (2) presented the total cost of the green

cement product reached about (28181559041)

dinars with eliminating waste of kiln dust by

recycling, which amounted to (50716547821)

dinars. The production of 744,723 tons of green

cement requires (500,750) tons of clinker instead

of (649754) tons of clinker in the production of

resistant cement, and this led to a decrease in the

need for raw materials (putty) entering the rotary

kiln.

The production of 744,723 tons of green

cement requires (500,750) tons of clinker instead

of (649754) tons of clinker in the production of

resistant cement, and this led to a decrease in the

need for raw materials (putty) entering the rotary

kiln .

The cost of producing line was (50716547821

dinars) according to the material flow cost

accounting, the cost per ton (68100

dinars/ton).While the cost of producing green

cement-CKD type is (28181559041 dinars),

according to the innovation of the green product.

Green Innovation within Materials Flow Cost: Opportunities and Challenges

25

Table 2: The follow Costs within green product innovation.

Input Output green cement product

cost elements Quantity (Ton) cost (Dinar) Quantity (Ton) cost (Dinar)

first stock 9154 15055444

Quantity of green cement received 700795 90195551054 - -

sachet packaging materials 1501014 9141119444 - -

other stock 145 15055444 - -

User of material - 99155955054 077070 91491579941

Power electricity 5728421

Kwh

0951459 - -

133200 liter 99455515 - -

System - 9979491990 - -

total cost of bagged and free gree

n

cement

91919551409 077070 91491579941

3 CONCLUSIONS

The study aimed to identify the application of

material flow cost accounting in light of green

product innovation. For the purpose of producing

green cement in the national company of Cement

industry. Depending on quantitative income,

reached the need to adopt modern technologies

such as accounting for material flow costs, green

product innovation and other modern techniques to

address the sharp rise in costs experienced for the

companies by increasing efficiency in resource

exploitation and improving the decision-making

process for continuous improvement, thus

improving production and environmental

performance At the same time, which achieves

economic benefits that affect the financial position

of the plant while achieving environmental

benefits. The study also urges the need to move

towards green innovation approach in all products

and processes in the factory that will enhance the

national product and not rely on imported foreign

products, as well as to be able to apply modern

systems and methods that remain in the face of

intense competition from local and imported

products Which filled the markets, he had to set up

training courses for all employees and workers, all

according to specialization, because high skills are

reflected on performance at work.

REFERENCES

Abdullah, M., Zailani, S., Iranmanesh, M., & Jayaraman,

K. (2016). Barriers to green innovation initiatives

among manufacturers: the Malaysian case. Review of

Managerial Science, 10(4), 683-709.

Bau mer-Cardoso, M. I., Campos, L. M., Santos, P. P. P.,

& Frazzon, E. M. (2020). Simulation-based analysis

of catalyzers and trade-offs in Lean & Green

manufacturing. Journal of Cleaner Production, 242,

118411.

Biswas, A., & Roy, M. (2016). A study of consumers’

willingness to pay for green products. Journal of

Advanced Management Science, 4(3).

Dekamin, M., & Barmaki, M. (2019). Implementation of

material flow cost accounting (MFCA) in soybean

production. Journal of Cleaner Production, 210,

459-465.

Farias, L. M. S., Santos, L. C., Gohr, C. F., & Rocha, L.

O. (2019). An ANP-based approach for lean and

green performance assessment. Resources,

conservation and recycling, 143, 77-89.

Huang, S. Y., Chiu, A. A., Chao, P. C., & Wang, N.

(2019). The application of Material Flow Cost

Accounting in waste reduction. Sustainability, 11(5),

1270.

Huang, X.-x., Hu, Z.-p., Liu, C.-s., Yu, D.-j., & Yu, L.-f.

(2016). The relationships between regulatory and

customer pressure, green organizational responses,

and green innovation performance. Journal of

Cleaner Production, 112, 3423-3433.

ISO14051, I. (2011). Environmental management-

Material flow cost accounting-General framework.

International Organization for Standardization,

Geneva.

ICFITM 2021 - INTERNATIONAL CONFERENCE ON FINANCE, INFORMATION TECHNOLOGY AND MANAGEMENT

26

Kokubu, K., & Nakajima, M. (2004). Material flow cost

accounting in Japan: A new trend of environmental

management accounting practices. Fourth Asia

Pacific Interdisciplinary Research in Accounting

Conference,

Syarif, A. M., & Novita, N. (2019). Environmental

management accounting with material flow cost

accounting: strategy of environmental management

in Small and Medium-sized Enterprises production

activities. Indonesian Management and Accounting

Research, 17(2), 143-167.

Sygulla, R., Götze, U., & Bierer, A. (2014). Material

flow cost accounting: a tool for designing

economically and ecologically sustainable

production processes. In Technology and

manufacturing process selection (pp. 105-130).

Springer.

Wahyuni, D. (2009). Environmental management

accounting: Techniques and benefits. Jurnal

Akuntansi Universitas Jember, 7(1), 23-35.

Green Innovation within Materials Flow Cost: Opportunities and Challenges

27