Research on Internal Audit Capability of Universities based on SPSS

Model

Chengying Zhang*

a

and Jiawen Zhu

b

School of Management, Xihua University, Chengdu, China

Keywords: Universities, Internal Audit, Governance Capacity, Modernization.

Abstract: As an important branch of the national internal audit system, internal audit in colleges and universities plays

an extremely important role in promoting the improvement of teaching quality, anti-corruption and anti-

corruption, and regulating the education and teaching system. However, at present, there are mainly problems

such as unsound internal audit program, insufficient audit capability, and not widely applied audit information

technology in replacement colleges and universities, which seriously restrict the role of internal audit. Based

on this, this paper spss data analysis model as the basis, on the basis of analyzing the linear relationship

between university internal audit and university governance, focuses on the proportion and relevance of

university internal audit in the university governance system, and finally puts forward the guarantee measures

to play the role of internal audit governance in public universities. The study has a non-negligible role for the

related research in the field of modernization of university governance.

1 INTRODUCTION

The concept of governance began in the 1990s and

was gradually introduced to the field of education

with the development of the times. Governance in

higher education is the sum of all activities and

processes to transform the traditional management

system and order system of higher education in

accordance with the concept, principles and methods

of governance with social values as the goal. In the

background that the actual right to run and found the

university is separated, university governance is a

kind of institutional arrangement that regulates and

restrains the exercise of power, so that the university,

government and society and other stakeholders can

interact harmoniously and jointly govern the

university (Zhao, Gao, 2018). The purpose is to build

a clean, efficient and balanced governance system to

improve the scientific research level and talent

cultivation quality of colleges and universities,

regulate the bad behaviors of related subjects, and

guarantee the equal power and interests of all parties

involved in governance. Nowadays, with the

continuous advancement of economic globalization

a

https://orcid.org/0000-0002-1427-9669

b

https://orcid.org/0000-0002-7453-6540

and knowledge integration process, the Party has put

forward higher requirements for all aspects of

replacement education, which makes internal

auditing in colleges and universities face

unprecedented opportunities and challenges (Zhuang,

Guan, 2016). In the new era, internal audit of colleges

and universities should be bold to remove the old and

establish the new, seek development in the midst of

change, give full play to the role of internal audit as a

constraint, supervision and promotion, and escort for

the modernization of governance ability of colleges

and universities.

2 THE RELATIONSHIP

BETWEEN INTERNAL AUDIT

AND UNIVERSITY

GOVERNANCE

2.1 System of University Governance

The internal governance system of colleges and

universities refers to the fact that in order to achieve

Zhang, C. and Zhu, J.

Research on Internal Audit Capability of Universities based on SPSS Model.

DOI: 10.5220/0011172300003440

In Proceedings of the International Conference on Big Data Economy and Digital Management (BDEDM 2022), pages 227-232

ISBN: 978-989-758-593-7

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

227

the goal of building a world-class college with

Chinese characteristics, public colleges and

universities should adhere to social and spiritual

values as the basic value orientation, take the

institutional restraint and incentive system formed by

the joint action of formal system and informal system

as the core, and take the decision-making,

implementation (Li 2020), participation and

supervision as the basic action mode within the

school, through the synergy and interaction of all

parties in college governance so as to A good order

system is formed through the interaction of all parties

of university governance. The internal governance

system of colleges and universities is the basic carrier

of college governance activities and the means and

methods to realize "good governance" in colleges and

universities, which is the institutional innovation and

mechanism innovation different from the traditional

internal management of colleges and universities.

2.2 Relationship between Internal

Audit and Governance of Colleges

and Universities

Internal audit is born in the governance system of

colleges and universities and assumes the function of

evaluating and supervising the governance structure

and system as well as governance effect of colleges

and universities (Wang 2021). It is an indispensable

warning sign in university governance. On the one

hand, internal audit can regulate the bad behavior of

related subjects and prevent potential risks in time to

achieve the effect of governance through its

supervision function. On the other hand, due to its

top-down nature and the participation of multiple

subjects, university governance enables internal audit

department to carry out audit work relatively

independently under a better moral restraint

environment.

3 THE STATUS AND ROLE OF

INTERNAL AUDIT IN THE

GOVERNANCE SYSTEM OF

COLLEGES AND

UNIVERSITIES

3.1 The Status of Internal Audit in

University Governance System

The top-down structure of university governance

system is mainly divided into decision-making level

and executive level, and internal audit belongs to the

executive level like research centers and departments,

but it also belongs to the supervisory level. Internal

audit is under the direct leadership of the president,

which greatly avoids conflicts of interest with other

departments in the executive level, and thus has a

strong independence to re-monitor the

implementation of the executive level and give full

play to its supervisory and control role.

3.2 The Role of Internal Audit of

Colleges and Universities in the

Governance System of Colleges and

Universities

As an important part of the internal control

mechanism of colleges and universities, internal audit

of colleges and universities plays an important role in

monitoring the utilization of limited resources of

schools, realizing the reasonable allocation of

educational resources and improving the

modernization of school management. Sound internal

audit can timely and accurately find out the problems

in the operation of universities and give early warning

and suggestions. Especially with the development of

the strategy of replacing education to develop the

country, the state financial support for the

development of education has been increasing. Under

this new situation, the role of reasonable and effective

internal audit is more and more important in the

management of fund budget, improving the

efficiency of resource utilization, controlling internal

risks and evaluating economic responsibility.

4 RESEARCH ON INTERNAL

AUDIT ISSUES OF COLLEGES

AND UNIVERSITIES BASED

ON CASE STATISTICS

4.1 Statistics of Internal Audit Cases in

Colleges and Universities in

Sichuan Province

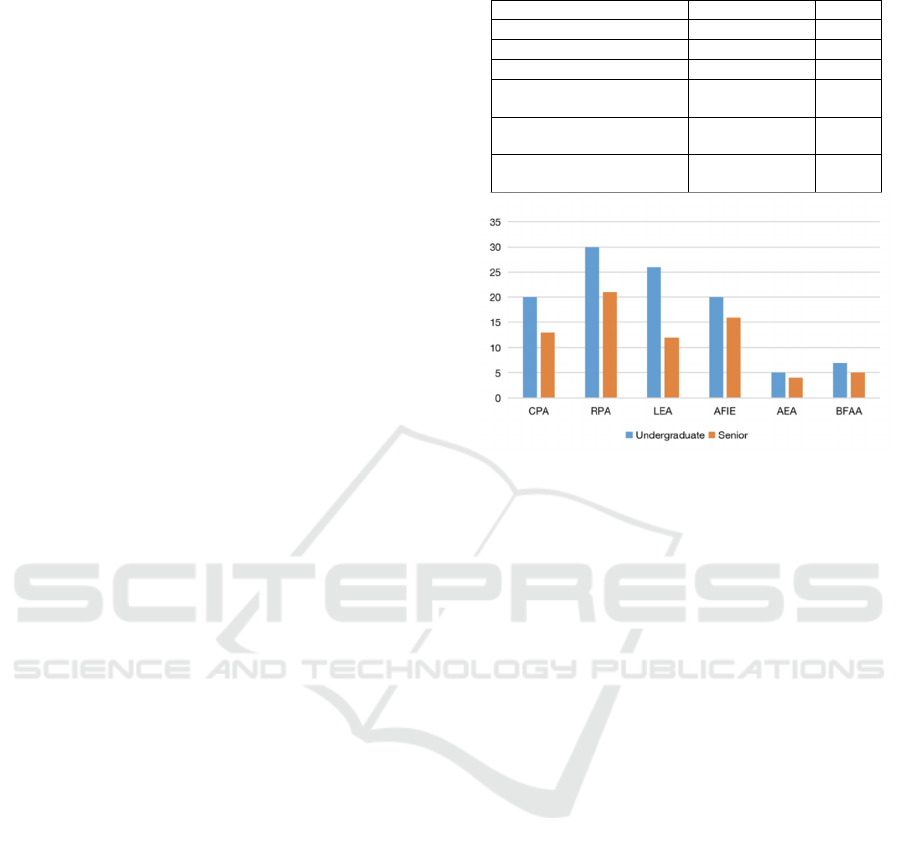

Capital construction project audit and repair project

audit: 20 undergraduate colleges and universities

conducted capital construction project audit in 2019,

and completed more than 370 items of capital

construction project audit; 30 undergraduate colleges

and universities conducted repair project audit, and

completed more than 2160 items of repair project

audit (Ma 2021). There are 13 institutions of higher

BDEDM 2022 - The International Conference on Big Data Economy and Digital Management

228

education conducting capital construction audits and

completing more than 50 audits of capital

construction projects; there are 21 institutions of

higher education conducting audits of repair projects

and completing more than 620 audits of repair

projects. The sample colleges and universities have

completed more than 3,000 audits of capital

construction projects and renovation projects

throughout the year, with the amount of audits sent

reaching 1.763 billion yuan and 222 million yuan of

reductions.

Economic responsibility audit of leading cadres:

In 2019, 26 undergraduate institutions carried out

economic responsibility audit of middle-level leading

cadres and completed a total of 226 economic

responsibility audit projects; 12 senior high schools

carried out economic responsibility audit of middle-

level leading cadres and completed a total of 51

economic responsibility audit projects.

Financial revenue and expenditure audits: 20

undergraduate institutions conducted financial

revenue and expenditure audits in 2019, completing a

total of 117 financial revenue and expenditure audit

projects; 16 senior high schools conducted financial

revenue and expenditure audits, completing a total of

50 financial revenue and expenditure audit projects.

Special audit investigation of educational

economic activities: taking into account the actual

situation of each university, a total of 370 special

audit investigations were conducted in 2019, mainly

on the audit supervision of education fee charging

behaviors, scientific research fund use and financial

management of canteens with high risk of integrity.

In the same year, the Provincial Department of

Education organized internal auditors of some

universities to carry out special audit investigations

on the management and use of scientific research

funds and discipline construction funds of 5

universities. At the same time, the universities also

generally carry out auditing and signing work on

scientific research funds.

Financial budget execution and final accounts

audit: in 2019, 7 undergraduate colleges and

universities carried out financial budget execution

and final accounts audit, completing a total of 20

financial budget execution and final accounts audit

projects; 5 higher vocational colleges and universities

carried out financial budget execution and final

accounts audit, completing a total of 32 financial

budget execution and final accounts audit projects.

Table 1: Audit project statistics table.

Audit Projects Undergraduate Senior

Capital Project Audits 20 13

Renovation Project Audi

t

30 21

Leading Economic Audits 26 12

Audit of financial income

and expenditure

20 16

Audit of Educational

Activities

5 4

Budget and final account

audits

7 5

Figure 1: Audit Project Statistics Chart.

4.2 Research on Existing Problems

Insufficient attention to internal audit in colleges and

universities: Some colleges and universities internal

audit departments are nominally under the direct

leadership of principals or party secretaries, but in

reality, they will arrange other vice principals to

manage directly, lacking audit authority; some

colleges and universities have audit system, but there

are problems such as auditors are not familiar with

audit system and audit system is not in place; some

colleges and universities audit has become a

subsidiary organization of discipline inspection and

supervision, and audit Some colleges and universities

have audit become subsidiary organizations of

discipline inspection and supervision, and the audit

department does not have enough independence. The

above situation from the side reflects that the

management of colleges and universities does not pay

enough attention to the audit department

(Yang 2021).

In reality, some colleges and universities have

internal audit institutions, but due to the unsound

institutional settings, there is a situation that audit and

discipline inspection and supervision departments

work together, and even the audit department is

directly listed in other departments. Internal auditors

lack independence. As internal staffs of colleges and

universities, their personnel relations are still under

the system of colleges and universities, so they are

easily restricted by the system and policies of

colleges and universities, and there are complex

Research on Internal Audit Capability of Universities based on SPSS Model

229

interpersonal circles in colleges and universities,

which are easily influenced by human feelings and

worldly affairs, which to a certain extent also lead to

the lack of independence of auditing work.

The internal auditing system of colleges and

universities is not perfect: Although the relevant

guidelines for the construction of internal auditing

system of colleges and universities have been issued

at the national level, very few colleges and

universities integrate it with their actual situation. At

present, some universities still lack basic systems

such as economic responsibility audit and internal

audit work regulations.

There is a shortage in the supply of human

elements with higher ability level: At present, the

internal audit team of Chinese universities generally

has a single knowledge structure, insufficient ability

and insufficient number of personnel, which makes it

difficult to offer constructive opinions on the

problems encountered in the audit process in time,

and the overall quality of the team fails to meet the

development needs of university governance, which

greatly affects the audit quality.

The means of internal audit in colleges and

universities are relatively backward: At present, most

colleges and universities still adhere to traditional

audit methods, due to the small investment in capital,

technology and talents, which leads to the less

application of information technology. The current

auditing methods are backward, lack of necessary

funds and technical support, backward information

construction, low sharing of audit information and

resources, and serious information "silo"

phenomenon, which leads to low audit efficiency and

uneven audit results.

5 SAFEGUARD MEASURES TO

UTILIZE THE ROLE OF

INTERNAL AUDIT

GOVERNANCE IN PUBLIC

UNIVERSITIES

5.1 Adhere to the Leadership of the

Party to Improve the Audit Work

Environment

The newly revised Internal Audit Department Order

No. 11 of January 12, 2018 clearly puts forward that

"the internal audit organization shall carry out audit

work under the direct leadership of the party

organization and the main person in charge of the

unit", emphasizing the importance of the party

leading the audit work. Universities should accelerate

the establishment of a sound system of internal audit

mechanism under the leadership of the party

committee and set up an audit committee to be

responsible for making audit plans, listening to audit

reports and dealing with irregularities and violations.

At the same time, the party committee of colleges and

universities should give full play to its role of

coordinating all parties, handle the relationship

between audit work and other work, actively mobilize

relevant departments to cooperate with the

audit work,

and create a good atmosphere for internal audit.

5.2 Enhancing the Independence of

Internal Audit Work

First, the independence of the internal audit

organization is a prerequisite for internal auditors to

carry out objective and impartial auditing work.

Therefore, a separate audit department must be

established to clearly regulate the scope of audit work

and avoid the involvement of the audit department in

the economic activities of the school, which affects

the quality of audit work. Second, audit staff should

not be involved in the specific work of other

departments, such as financial management,

accounting, or other production, operation, or

management activities. They should not have

economic interests with the main person in charge of

the audited department. The audit staff should strive

to be clean, independent and objective, without

yielding to any threats or making any compromises

that would lower the quality of the audit, and inspect

and supervise the work of each department from an

objective and impartial third-party perspective. Third,

in the process of audit plan formulation,

independence is maintained regarding the

determination of audit techniques, procedures, and

application scope; in the stage of audit plan

implementation, independence is maintained

regarding the determination of audit policies, audit

objects, and audit scope; in the stage of presenting

audit reports, independence is maintained regarding

the presentation of audit results and the presentation

of opinions and recommendations.

5.3 Improve Internal Audit System and

Strengthen the Supervision of

System Implementation

Establishing a sound internal audit system in colleges

and universities is conducive to improving the

efficiency and quality of internal audit work. Based

BDEDM 2022 - The International Conference on Big Data Economy and Digital Management

230

on the original auditing system, universities should

make more specific auditing specifications according

to the setting of school units and the actual situation

of school economic activities, so as to clarify the

scope, subject, content, process and implementation

method of auditing work and further standardize the

auditing procedures. In a word, we should make the

auditing work lawful, lawful, strict and illegal in

order to give full play to the supervisory role of

internal audit in colleges and universities. Clarify the

work positioning of internal audit in university

governance, establish and improve the mechanism of

supervision, accountability, discipline and error

correction for the implementation of internal audit

system in universities, and continuously improve the

construction of university governance system.

Establishing and improving the effective feedback

mechanism of system implementation is the only way

to give feedback to the problems arising in the

process of implementation of internal audit system in

colleges and universities, so as to promote the

adjustment and optimization of the system.

5.4 Build a Composite Audit Team and

Enhance Internal Audit Capability

Strive to build a high-quality professional internal

audit team: universities should give full play to the

advantages of talents and cultivate a professional

audit team with strong belief, proficient in business

and excellent style. First, strengthen the professional

ethics education of auditors. The characteristics of

internal audit work determine that auditors must have

high audit professional ethical quality and political

quality. Always maintain integrity, resist corruption,

and prevent interference in the audit work from the

external environment. Objective and fair handling of

audit issues, make recommendations to ensure the

normal operation of the school's economic work and

safeguard the interests of the school. Second, improve

the level of business knowledge and ability of

auditors. Develop a long-term plan for the

development of the audit team. Auditors themselves

should also establish a "lifelong learning" thinking,

and actively participate in higher training, take the

initiative to learn new knowledge, constantly update

the knowledge base, only their professional

knowledge is excellent, in order to better serve the

audit work. Third, to strengthen the follow-up

education of auditors, auditors at least once a year to

participate in continuing education and training.

Through political learning and business learning or

send personnel to participate in various audit training

courses, learning audit theory, policies and

regulations, professional ethics education. "Training

by audit", dispatching personnel to participate in

auditing institutions and relevant departments on

campus audit, inspection work, and constantly

improve the ability of auditors to adapt to the integrity

of governance.

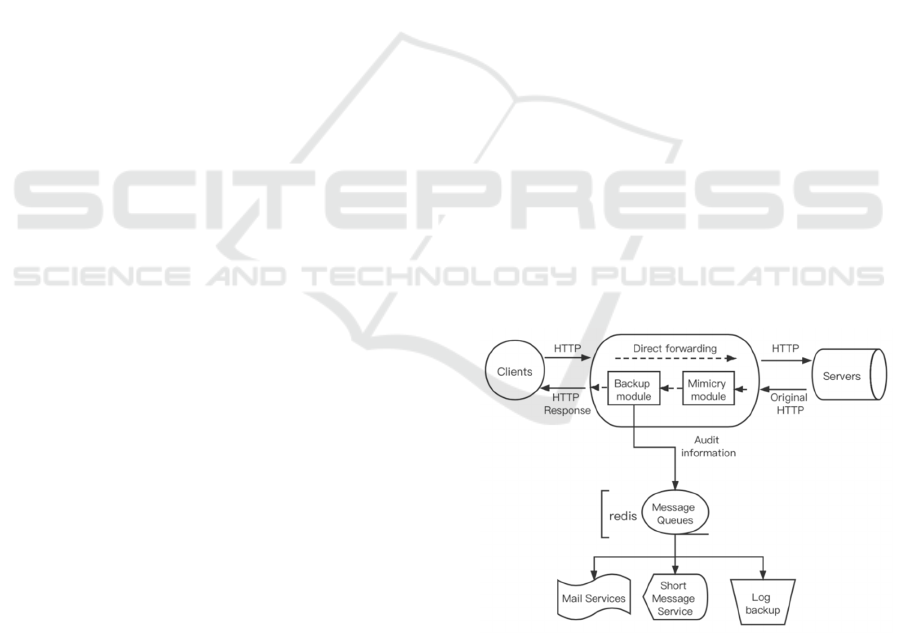

5.5 Improve the Means of Internal

Audit Informationization in

Colleges and Universities

Firstly, internal audit workers in universities should

make good departmental budgets, strive for more

financial input, prepare comprehensive and complete

scientific and compliant budget statements, and strive

for more special funds for the introduction of

advanced auditing techniques. Secondly, the

application of information technology should be

strengthened. Universities should accelerate the

combination of information technology and auditing

technology, such as computer-aided auditing,

artificial intelligence and networked auditing, to

innovate the concept of auditing and change the

traditional auditing methods. Finally, a network

infrastructure platform featuring cloud computing

and mobile terminals should also be built as a way to

collect data and conduct early warning analysis so as

to better play a supervisory role. Traditional audit

methods and modern audit technology tools are fully

integrated to build on their strengths and avoid their

weaknesses, thus maximising audit efficiency and

quality levels.

Figure 2: Smart Audit System Flow Chart.

6 CONCLUSION

Facing the new historical opportunities and

challenges, colleges and universities should fully

Research on Internal Audit Capability of Universities based on SPSS Model

231

realize the important role of internal audit in

supervising, evaluating and advising the governance

system of colleges and universities, regulating the

business activities of colleges and universities, and

improving the construction of internal control. The

only way to give full play to the role of audit

supervision and service and promote the healthy and

sustainable development of universities and the

modernization and improvement of governance

ability is to adhere to the Party's leadership and keep

pace with the times, continuously improve the

internal audit mechanism and system, cultivate a

high-quality professional audit team and innovate the

methods and means of audit work.

REFERENCES

Li Guofei. Research on the ways of internal audit playing

an important role in serving university governance.

Education and Teaching Forum. 2020(32):354-355.

Ma Qiqi. Problems and optimization measures of internal

audit work in colleges and universities. Investment and

Cooperation,2021(11):38-39.

Wang Bin. Discussion on the problems of internal audit in

colleges and universities and strategies to cope with

them . Business News,2021 (30): 148-150.

Yang Hui. How to strengthen the information construction

of internal audit in universities under cloud audit. Hebei

Enterprise,2021(11):76-78.

Zhao Xianning,Gao Yan. The development status, dilemma

and optimization of replacing internal governance in

universities. Heilongjiang Higher Education

Research,2018,36(06):69-72.

Zhuang Li, Guan Xiaomin. Research on internal audit

based on university governance system. Journal of

Minnan Normal University: philosophy and social

science edition, 2016, 30(4):5.

BDEDM 2022 - The International Conference on Big Data Economy and Digital Management

232