Research on the Influence of Equity Pledge of Controlling

Shareholders on Enterprise Innovation: Based on the Real Surplus

Management Perspective

Guangqiang Han and Yingxue Wang

School of Economics, Bohai University, Jinzhou, Liaoning, China

Keywords: Equity Pledge, Real Surplus Management, Enterprise Innovation, Mechanism Analysis, Intermediary Effect.

Abstract: The article samples Chinese A-share listed companies from 2007 to 2020, and verifies the relationship

between the controlling shareholder equity pledge, surplus management and enterprise innovation by using

empirical research methods. The study found that the implementation of equity pledge by the controlling

shareholders will reduce the degree of innovation of enterprises, and the real surplus management will play a

partial intermediary role in the relationship between the two. The research conclusion is helpful to improve

the economic consequence theory of equity pledge.

1 INTRODUCTION

The Fifth Plenary Session of the 19th CPC Central

Committee proposed that the 14th Five-Year Plan

period must be innovation-driven and high-quality

supply. Although research and innovation will lead to

a large increase in enterprise costs in the short term,

it is related to the long-term development of

enterprises. According to the statistics of wind

database, as of November 26,2021, the number of

pledged shares in the A-share market is 429.87 billion

shares, and the equity pledge situation is generally

more common. When the controlling shareholder

makes a large proportion of the equity pledge to

finance, motivated to maintain control, it tends to use

its own control for various surplus management

activities, so as to stabilize the stock price. Cutting

innovation investment is an effective method of real

surplus management.

Some scholars have analyzed the relationship

between equity pledge and enterprise innovation

from the perspective of internal control, management

risk preference and institutional environment. From

the perspective of real surplus management, this

paper discusses the impact of equity pledge on

enterprise innovation, which provides a richer

perspective.

2 LITERATURE REVIEW AND

HYPOTHESES

AREPRESENTED

2.1 Equity Pledge and Enterprise

Innovation

Most scholars believe that equity pledge and

enterprise innovation are a linear negative

correlation. For example, Zhang Ruijun et al (2017)

believe that the negative relationship between the

controlling shareholder equity pledge and the

enterprise R & D investment (Zhang, et al, 2017),

while Li Changqing et al (2018) believes that such

will only occur when the equity pledge rate is higher

and the closer to the liquidation line (Li, et al, 2018).

Wenwen et al. (2018) believe that the equity pledge

of the controlling shareholders in the high-tech

industry has a stronger inhibitory effect on enterprise

innovation than (Wen, et al, 2018).Some scholars

believe that the relationship between the two is

nonlinear. Xu Weilong et al (2020) believe that with

the increase of the pledge ratio, the innovation ability

increases first and then reduces the (Xu, et al, 2020).

Based on this, we propose the hypotheses 1a,1b:

H1a: Equity pledge of major shareholders is

negatively related to enterprise innovation.

510

Han, G. and Wang, Y.

Research on the Influence of Equity Pledge of Controlling Shareholders on Enterprise Innovation based on the Real Surplus Management Perspective.

DOI: 10.5220/0011188900003440

In Proceedings of the International Conference on Big Data Economy and Digital Management (BDEDM 2022), pages 510-514

ISBN: 978-989-758-593-7

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

H1b: Equity pledge of major shareholders and

enterprise innovation is not a linear negative

relationship.

2.2 Equity Pledge and Surplus

Management

Surplus management activities are a relatively

common legal market value management behavior in

listed companies, which is divided into accrued

surplus management and real surplus management.

Sun Haitao et al. (2020) believe that the companies

that make the equity pledge will take more real

surplus management activities to adjust the surplus

(Sun, et al, 2020). Li Xiaodong et al (2020) also

believe that the equity pledge of major shareholders

is significantly negatively related to the degree of

accrued surplus management, and significantly

positively related to the degree of real surplus

management(Li, et al, 2020).The equity pledge of the

controlling shareholder that has been released within

the year has no significant impact on the real surplus

management degree of the company (Xie, et al, 2018)

.Based on this, the hypothesis 2 is proposed:

H2: The equity pledge of major shareholders has

a positive relationship with the real surplus

management.

2.3 Surplus Management and

Enterprise Innovation

Once the enterprise has the need for surplus

management activities, it will pay special attention to

the large expenses in the surplus management

activities. Long payback and costly R & D innovation

activities will be reduced by surplus management

activities. When the degree of surplus management is

reduced, the agency problems and financing

constraints are reduced, so that the enterprise

innovation behavior can be significantly improved

(Yu, et al, 2018). Businesses with R & D expenses

will engage in surplus management for real R & D

trading activities(Xiao, Zhou, 2012).The innovation

strategy of enterprises is divided into radical and

conservative types. The higher the real surplus

management degree of the enterprise, the lower the

intensity of its R & D expenditure, and the enterprise

will adopt a more conservative innovation strategy

(Dai 2016).

In general, equity pledge has led to an increase in

surplus management, and real surplus management

will be based on cutting corporate innovation. In this

way, the action path of "equity pledge, one real

surplus management and one enterprise innovation"

is formed. Thus, we propose the hypothesis that the

3:

H3: If H1a is established, the real surplus

management plays an intermediary role between

equity pledge and enterprise innovation.

3 RESEARCH DESIGN

3.1 Sample Selection and Data Sources

All the data in this paper are from GuoTai'an, and the

equity pledge data of major shareholders at the end of

2007-2020 is obtained through manual sorting.

Surplus management requires data from the previous

two years, which began in 2005.Excluding the

financial industry, missing data, and ST, *ST, and PT,

all continuous variables were processed with

Winsorize.

3.2 Variable-Definition

3.2.1 Explanatory Variable

The explanatory variable is the major shareholder's

equity pledge. According to the existing literature,

through the sorting of the pledge data of the current

year, the judgment standard is whether there is an

equity pledge by the major shareholder at the end of

the year, and the value is 1, and the value is 0. It does

not include the samples released in the current year.

Enterprises that did not update the pledge data in the

current year are consistent with the equity pledge in

previous years.

3.2.2 Explained Variable

The ratio of R & D investment and operating income

is taken as a measure of enterprise innovation:

Radint= Total enterprise R & D expenditure /

operating income

(1)

The larger the calculated Radint value indicates

that the higher the enthusiasm of the enterprise to

implement the enterprise innovation.

3.2.3 Mediating Variable

This paper uses real surplus management data from

GuoTaian database, represented by DREM. The

calculated DREM value is greater than zero and the

greater the degree of upward real surplus

management; the DREM value is less than zero and

Research on the Influence of Equity Pledge of Controlling Shareholders on Enterprise Innovation based on the Real Surplus Management

Perspective

511

the smaller, the higher the degree of downward real

surplus management.

3.2.4 Controlled Variable

Based on previous research results related to equity

pledge and earnings management, the following

variables are used as control variables: (1) Nature of

property rights (SOE): Based on whether it is a state-

owned enterprise, the value is 1 if it is a state-owned

enterprise, and 0 if it is not. (2) Shareholding ratio of

the largest shareholder (Top1): This variable is used

to represent the concentration of ownership. It is

measured by the proportion of the shares held by the

largest shareholder to the total shares of the listed

company. Generally, the larger the proportion, the

higher the degree of equity concentration. (3) Audit

quality (Big4): The Big Four accounting firms are

relatively authoritative accounting firms. It is

measured according to whether the listed company is

audited by the Big Four accounting firm at the end of

the year. (4) Size of the company (Size): The size of

the company is measured by taking the natural

logarithm of the company's total assets. The larger the

indicator is, the larger the company is. (5) Growth

rate of operating income (Growth): It is used to

express the development ability of the enterprise. It is

measured by dividing the operating income of the

current year by the operating income of the previous

year and subtracting one. (6) Number of directors

(Board): Indicates the size of the board of directors of

the listed company, which is measured by taking the

natural logarithm of the number of directors of the

company. (7) Tobin's Q value (Tobin): This variable

is used to measure the company's performance. It is

measured by the ratio of the company's market value

to the replacement cost of assets. At the same time,

two dummy variables of year and industry are defined

to control their effects.

3.3 Model Specification

In this paper, the stepwise test method of mediation

test is used to test whether the total effect coefficient

is significant, that is, whether there is a significant

relationship between the independent variable and the

dependent variable. If significant, proceed to

subsequent analyses, if not, mediation analysis is

terminated. Test whether the effect of the

independent variable acting on the mediating variable

is significant; if it is significant, continue the

subsequent test, otherwise stop the analysis, and the

mediating effect does not exist; test whether the effect

of the mediating variable acting on the dependent

variable is significant; if significant, continue the

subsequent test, otherwise stop the analysis, the

mediating effect does not exist; test whether the direct

effect is significant. When the first two items are

significant, if it is not significant, there is a complete

mediation effect (Judd, Kenny, 1981), otherwise

there is a partial mediation effect (Baron & Kenny

1986).

The following models are set up to conduct the

mediation effect test of assumptions 1,2 and 3, and

then use the Bootstrap method if the step-wise test is

not significant.

Hypothesis 1a、1b was verified to construct the

following multiple linear regression model:

Radinti, t=β0+β1Pledgei, t+β2Soei, t+β3Roai,

t+β4Top1i, t+β5Big4i, t+β6Sizei, t+β7Growthi,

t+β8Boaedi, t+β9Tobini, t+∑Y+∑IND+ε (2)

Hypothesis 2 was verified to construct the

following multiple linear regression model:

Pledgei, t=β0+β1DREMi, t+β2Soei, t+β3Roai,

t+β4Top1i, t+β5Big4i, t+β6Sizei, t+β7Growthi,

t+β8Boaedi, t+β9Tobini, t+∑Y+∑IND+ε (3)

To verify hypothesis 3, the following multiple

linear regression model was constructed by

combining the models (2) and (3):

Radinti, t=β0+β1Pledgei, t+β2DREMi, t+β3Soei,

t+β4Roai, t+β5Top1i, t+β6Big4i, t+β7Sizei,

t+β8Growthi, t+β9Boaedi, t+β10Tobini,

t+∑Y+∑IND+ε

(4)

4 EMPIRICAL ANALYSIS

4.1 Descriptive Statistics

The descriptive statistics of the variables in this paper

are shown in Table 2. The minimum value of R & D

investment of listed companies is 0, and the

maximum value is 251.6%. It can be seen that there

is a large gap in the innovation level of different listed

companies, and there is an extreme phenomenon of

excessive innovation investment in that year. For

example, in Junshi Biology in 2019 and 2020, this

value reached 122.06% and 112.72%. The median is

3.4%, indicating that the overall innovation level of

listed companies is low, and the innovation impetus

is insufficient. The average equity pledge ratio

(Pledge) of controlling shareholders is 44.5%,

indicating that the equity pledge situation of

controlling shareholders of listed companies is

relatively common.

The Variance Inflation Factor test refers to the

ratio of the variance when there is multicollinearity

BDEDM 2022 - The International Conference on Big Data Economy and Digital Management

512

among the explanatory variables to the variance when

there is no multicollinearity between the explanatory

variables. The larger the VIF, the more serious the

collinearity is. The judgment method shows that

when 0<VIF<10, there is no multicollinearity among

the variables. It can be seen from Table 3 that after

the VIF test, the VIF values of each variable (dummy

variable year, industry controlled) are all less than 2,

and it can be judged that there is no multicollinearity

between the variables.

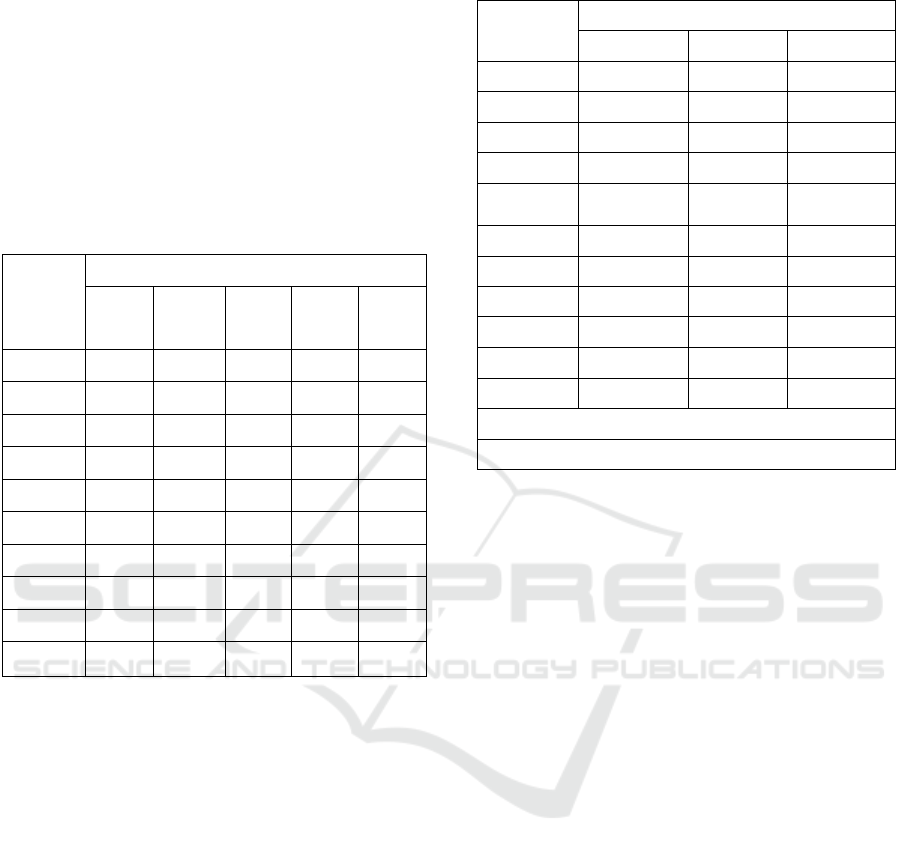

Table 1: Descriptive statistics.

Variable

Descriptive Statistical Items

Mean Median SE Min Max

Radint 0.044 0.034 0.054 0.000 2.516

Pledge 0.445 0.000 0.497 0.000 1.000

DREM -0.002 0.009 0.165 -0.652 0.496

SOE 0.344 0.000 0.475 0.000 1.000

Top1 0.335 0.316 0.137 0.085 0.729

Big4 0.048 0.000 0.213 0.000 1.000

Size 22.202 22.044 1.177 19.982 26.190

Growth 0.146 0.105 0.296 -0.493 2.276

Boar

d

2.150 2.197 0.169 1.792 2.708

Tobin 2.018 1.660 1.125 0.860 8.391

4.2 Regression Analysis

The first column of Table II reports the regression

results of the equity pledge on the innovation input

and innovation output of the first controlling

shareholder, with the regression coefficient of -0.003

at the 1% level, supporting the assumption of

H1a.The second column of Table II reports a

significant positive correlation between the equity

pledge of major shareholders and the real surplus

management at 1%, with a coefficient of 0.025,

supporting the assumption of H 2.In the third column

of Table II, after adding surplus management, equity

pledge and enterprise innovation are significantly

negatively related at 5%, and the coefficient

becomes-0.002; real surplus management and

enterprise innovation at 1%, with the coefficient of-

0.022, indicating that surplus management plays part

of the intermediary between equity pledge and

enterprise innovation. Taken together, the regression

results support the hypothesis of H 3 that there is a

partial mediation effect.

Table 2: Regression analysis.

Variable

Regression Analysis Results

Radint DREM Radint

Pledge -0.003*** 0.025*** -0.002**

(0.001) (0.003) (0.001)

DREM

-0.022***

(0.002)

controlled

variable

control control control

yea

r

control control control

trade control control control

constant 0.091*** 0.189*** 0.095***

(0.010) (0.035) (0.010)

observes 17,780 17,780 17,780

R-square

d

0.239 0.068 0.243

Standard errors in

p

arentheses

***

p

<0.01, **

p

<0.05, *

p

<0.1

5 RESEARCH CONCLUSIONS

AND RECOMMENDATIONS

5.1 Research Conclusions

This paper uses the data of A-share listed companies

for empirical analysis, and the following research

conclusions: the larger the equity pledge ratio of the

major shareholders, the higher the surplus

management degree, the less sufficient funds to

invest in research and development; or reduce R & D

expenditure through surplus management, the

enterprise innovation cannot be effectively

implemented.

5.2 Recommendations

Relevant countermeasures and suggestions in this

paper can be put forward from the following aspects:

First, listed enterprises should try to diversified

financing methods. Although equity pledge is a fast

and efficient financing method, financing through

equity pledge has risks. Enterprises should try

diversified financing methods to reduce the risk of

drastic fluctuations in enterprise stock prices.

Secondly, the listed enterprises should reduce the real

surplus management activities. We should give full

play to the role of internal and external supervision of

enterprises, ensure that the quality of surplus

Research on the Influence of Equity Pledge of Controlling Shareholders on Enterprise Innovation based on the Real Surplus Management

Perspective

513

information is at a relatively high level, and improve

the sustainability of enterprise development. Finally,

listed enterprises should maintain or even increase

their innovation efforts. For the long-term

development of enterprises, only continuous

innovation can have the competitiveness of the long-

term development of the enterprise. Only by making

continuous innovation, keeping up with or even

leading the trend of continuous change of the industry

can we maintain the long-term development of the

enterprise.

REFERENCES

Baron, R. M., & Kenny, D. A. (1986) The moderator-

mediator variable distinction in social psychological

research: Conceptual, strategic and statistical

considerations. Journal of Personality and Social

Psychology, 51: 1173-1182.

Deren, X., Ke, L. (2018) Equity pledge of the controlling

shareholder and the real surplus management of the

listed company. J. Accounting Research, 39: 21-27.

Hailian, X., Meihua, Z. (2012) R & D Spending and

Surplus Management —— is based on empirical

evidence of R & D accounting policy changes [J].

Securities Market Guide, 22:48-54.

Haitao, S., Kexin, W., Yueyue, H. (2020) Influence of

major shareholder equity pledge on real surplus

management —— is based on enterprise strategic

perspective. J. Friends of the Accounting, 38: 67-74.

Judd, C. M., & Kenny, D. A. (1981) Process analysis:

estimating mediation in treatment evaluations.

Evaluation Review, 5: 602–619.

Lianchao, Y., Weiguo, Z., Qian, B. (2018) Does surplus

information quality affect enterprise innovation? [J].

Modern Finance and Economics (Journal of Tianjin

University of Finance and Economics), 38: 128-145.

Ruijun, Z., Xin, X., Chao'en, W. (2017) Major shareholder

equity pledge and enterprise innovation. J.Audit and

Economic Research, 32: 63-73.

Weilong, X., Yue, P. (2020) Study on the influence of

shareholder equity pledge on the innovation ability of

enterprises [J]. Science and technology promotes

development, 16 (12): 1603-1611.

Wen, W., Yinmo, C., Yuting, H. (2018) Research on the

Impact of Controlling shareholder Equity Pledge on

Enterprise Innovation. J. Journal of Management, 15:

998-1008.

Xia, D. (2016) Real Surplus Management with R & D

expenditure —— a GEM listed company Experience

Evidence [J]. Technology management research, 36

(04): 224-228.

Xiaodong, L., Key, Z., Jin, W. (2020) Equity pledge of

major shareholders, internal control and surplus

management [J]. Friends of the Accounting, (24): 75-

83.

BDEDM 2022 - The International Conference on Big Data Economy and Digital Management

514