Internal Audit of the Business Partner’s Reliability for Sustainable

Development of the Enterprise

Ruslan Dutchak

1a

, Olha Kondratiuk

1b

, Olena Rudenko

1c

, Andrii Shaikan

1d

and Rustem Adilchaev

2e

1

State University of Economics and Technology, Department of Accounting and Taxation, street Medical 16,

Kryvyi Rih 50000, Ukraine

2

Karakalpak State University named after Berdakh, Department of Economics, Nukus 1, Ch. Abdirov street,

Nukus, 230100, Uzbekistan

Keywords: Internal Audit, Sustainable Development, Reliability, Risk of Dishonesty, Business-Partner, Semantic Search,

Discretion of Choice.

Abstract: This article is concerned with the study of the problem of dishonesty of business-partners in the sustainable

development of enterprise and with the search of effective ways to solve it. The article reveals the essence of

the concept of business partner’s reliability, specifies its connection with the sustainable development of

enterprise, and shows the analysis of factors of the negative impact on such reliability. The main risks of

violation of the business partners’ reliability were identified and an assessment of possible problems (damage)

of enterprise due to interaction with a dishonest business partner was taken. It was grounded the applicability

of the internal audit for the careful choice by top management of a reliable business partner’s enterprise. The

internal audit method has been improved by additional involvement of modern systems of semantic search of

information on a business-partner in the Internet, inclusive in the state registers and data bases, electronic

mass media, social networks and other sources. The basic requirements for the competencies of internal audit

employees for a critical analysis of the risks of dishonesty of business partners and development of proposals

to avoid or minimize the negative consequences of existing risks have been determined.

1 INTRODUCTION

The main strategy for the development of mankind at

the beginning of the XXI century was the concept of

sustainable development, adopted by Resolution 70/1

of the General Assembly of the United Nations

“Transformation of our world: 2030 Agenda for

Sustainable Development” dated September 25, 2015

(UN, 2015). Clauses 18 and 59 of this Resolution

approve 17 global development goals of the countries

for the period from 2015 to 2030. The paradigm of

sustainable development has changed the traditional

understanding of economic growth to a new

theoretical and methodological model of balanced

economic development with the simultaneous

a

https://orcid.org/0000-0002-4837-068X

b

https://orcid.org/0000-0003-1000-0568

c

https://orcid.org/0000-0001-7293-7773

d

https://orcid.org/0000-0002-4088-6518

e

https://orcid.org/0000-0001-7598-6298

preservation of the ecology and solution of social

problems. The implementation of the indicated goals

requires global cooperation of all countries of the

world. Each country should take into account the

goals and objectives of sustainable development in its

strategic planning processes. A special place in the

state's achievement of sustainable development goals

belongs to its enterprises.

Sustainable enterprise development is a business

model that operates on the basis of profitability,

continuity, environmental friendliness and social

responsibility. Such development of the enterprise

requires its management to change traditional

approaches to the new object “business-ecology-

society”, what should be reflected in the distribution

Dutchak, R., Kondratiuk, O., Rudenko, O., Shaikan, A. and Adilchaev, R.

Internal Audit of the Business Partner’s Reliability for Sustainable Development of the Enter prise.

DOI: 10.5220/0011346200003350

In Proceedings of the 5th International Scientific Congress Society of Ambient Intelligence (ISC SAI 2022) - Sustainable Development and Global Climate Change, pages 155-166

ISBN: 978-989-758-600-2

Copyright

c

2022 by SCITEPRESS – Science and Technology Publications, Lda. All rights reserved

155

of finances, the definition of investment objects, the

choice of contracting parties, personnel policy, the

assessment of business performance indicators, non-

financial reporting, etc. Especially relevant for

management is the task of achieving continuity of

enterprise development in conditions of uncertainty.

The modern business environment for any

enterprise is extremely risky. The greatest source of

danger for the sustainable development of an

enterprise is its business partners. The main types of

problems that its business partners can create at the

enterprise are additional inspections of controlling

state bodies, court disputes, seizure of assets,

corruption scandals, sanctions of international

institutions, reputational losses, boycott, termination

of delivery chains, bankruptcy, conflicts with trade

union organizations, environmental pollution and

other. The moment of activation of the probability of

occurrence of the indicated problems at the enterprise

is the signing of a cooperation agreement with

business partners. The moment of the real problem is

the fact of a general business transaction (transfer of

funds, receipt and transfer of goods, works or

services) with a business partner. To minimize the

existing risks, the enterprise needs to make sure of the

business partner’s reliability, as a law-abiding partner

with moral and ethical owners, senior management

and staff. The enterprise management must achieve

this assurance till the moment of decision making

regarding the signing of an agreement with a

business-partner. In case of the long-term cooperation

with a business-partner under existing agreements,

the company must periodically review the observance

of the business partner’s reliability. To receive the

specified assurance, the enterprise management may

initiate a verification procedure for its business

partner’s reliability. The result of such a check

depends on the informational support for making a

management decision on safe cooperation with a

business partner. This means that an internal audit

unit must be created in the organizational and

management structure of a traditional enterprise, one

of the competencies of which will be the verification

of the business partner’s reliability.

The question regarding internal audit in the

modern scientific literature was reflected in the

researches of a wide variety of authors. The

conducted analysis of the last publications regarding

this question allows emphasizing of the main results

of such researches. Salagrama S. presented in his/her

article (Salagrama, 2021) a new model analysis

structure of the information security requirements for

the most reliable informational system and its assets

in the organizations. Abbas D. S., Ismail T., Taqi M.,

Yazid H. found in their research (Abbas et al., 2021),

that the availability at the enterprise of the authorized

persons for independence and internal audit makes a

significant positive influence on the transparency of

the financial reporting and improvement of the

enterprise’s reputation. Rahahleh M. H., Hamzah A.

H. B., Rashid N. (Rahahleh et al., 2021) explain how

an artificial intelligence can operate in the audit of

accounting information reliability, what allows to the

managing directors to receive the qualitative

accounting information and to relieve the

manipulations with incomes by means of the reduce

of informational risk. Handayani S., Kawedar W.

(Handayani & Kawedar, 2021) asserts that the inner

control is an effective factor for minimization of fraud

possibilities at the enterprise. De Capitani Di

Vimercati S., Foresti S., Paraboschi S., Samarati P.

(De Capitani Di Vimercati et al., 2020) offer an

approach for the safe use of cloud technologies to

ensure the implementation of internal control and

audit functions in corporate governance. Raji I. D.,

Smart A., White R. N., (...), Theron D., Barnes P.

(Raji et al., 2020) developed a structure for the

algorithmic audit, that supports end-to-end

development of an artificial intelligence system and

will be applied throughout the entire development life

cycle of an internal organization of enterprise.

According to the results of the study (Khersiat, 2020),

Khersiat O. came to the conclusion that internal audit

based on the COSO system has a very positive effect

on the transparent performance of tasks for the

insurance of reliability, improvement of quality and

efficiency in the municipality of Velykyi Amman.

Dutchak R., Kondratiuk O., Rudenko O., Shaikan A.,

Shubenko E. (Dutchak et al., 2021) grounded the

reasonability of the use of internal audit for the

system-based counteraction to the cybercrimes at the

enterprise and they improved the internal audit

method via additional involvement of tracking ways

for electronic (digital) traces of lawbreakers in the

enterprise’s cyberspace. Turker I., Bicer A. A.

(Turker & Bicer, 2020) proved in their study that the

use of a blockchain system in the audit process

improves the quality of the audit without increasing

the time spent on data checking. Mocanu M., Ciurea

C. (Mocanu & Ciurea, 2019) confirm that the internal

audit remains as an independent and objective activity

for provision of assurance, intended to increase in

value and improvement of organization’s activity.

Bondarenko T., Dutchak R., Kondratiuk O., Rudenko

O., Shaikan A., Shubenko E. (Bondarenko et al.,

2020) grounded the reality of the perspective of the

inner audit for resolving conflicts in enterprise

accounting, using the instruments of an artificial

ISC SAI 2022 - V International Scientific Congress SOCIETY OF AMBIENT INTELLIGENCE

156

intelligence (artificial neural networks and machine

learning). Korkushko O. N., Kushnir L. A.

(Korkushko & Kushnir, 2020) proved that the internal

audit service provides reliable protection of business

from errors and abusive activity, gives the possibility

to determine the “risk zones”, to identify and to

eliminate the gaps in the enterprise management

systems.

The conducted analysis allows us to deduce that

the matter of internal audit of the business-partner’s

reliability for the sustainable development of

enterprise does not have a systematic study. The

scientific literature has the researches of individual

fragments of this topic: internal audit, information

security, reliability, cloud technologies, artificial

intelligence, blockchain systems, cyberspace, etc.

The traditional method of internal audit does not meet

the modern management tasks for the sustainable

development of enterprise in a part of the checking of

the business partner’s reliability. Therefore, the

unresolved part of the identified problem remains the

lack of a systematic approach of internal audit for the

solution of the problem of the business partner’s

dishonesty for the sustainable enterprise’s

development.

The purpose of this article is to study the nature of

the phenomenon of the business partner’s reliability,

to evaluate the negative consequences (damage) from

interaction with a dishonest business-partner and the

development of the theoretical and methodological

provisions of internal audit for the enterprise

sustainable development.

To achieve these goals, the authors of this article

used the research methodology, which is based on the

dialectical method of cognition. At the same time, the

authors additionally used in the study the following

scientific methods: historical - in the study of trends

in the development of internal audit; analysis - in the

study of the components of sustainable development

of Ukraine, types of offenses in the field of economic

activity, components of indices; synthesis - when

determining the risks of the business partner’s

dishonesty, new competencies of employees and

methods of internal audit; abstraction - when

formulating negative consequences at the enterprise;

induction - when determining the impact of a

particular risk of the business partner’s dishonesty on

the general level of enterprise problems; deduction -

in the study of a system of symmetric search for

information about an individual business partner;

explanation - when revealing the content of a business

partner's reliability; classification - when determining

the types of risks of the business partner’s dishonesty;

systematization – when regulating the components of

the company's internal audit methodology;

concretization - when determining the methods of

harm causing to an enterprise due to the risks of the

business partner’s dishonesty; generalization - in the

preparation of internal documents for the use of

methods to collect and to analyze information about a

business partner in the practice of internal audit.

2 PRESENTATIONS OF THE

MAIN RESEARCH MATERIAL

2.1 Analysis of Sustainable

Development of Ukraine

According to clause 1 of the Decree of the President

of Ukraine “On the Sustainable Development Goals

of Ukraine for the period up to 2030” No.722/2019

dated 30.09.2019, Ukraine supported the global

sustainable development goals proclaimed by the

Resolution of the General Assembly of the United

Nations No. 70/1 dated 25.09.2015, and the results of

their adaptation, taking into account the specific of

development of Ukraine, presented in the National

Report “Goals of the sustainable development:

Ukraine”, to provide the compliance with the Goals

of the sustainable development (hereinafter referred

to as GSD) of Ukraine for the period till the year

2030:

1) poverty reduction;

2) overcoming hunger, achieving food security,

improving nutrition and promoting sustainable

agricultural development;

3) Insurance of healthy lives and promotion of

well-being for all at all ages;

4) provision of the integral and fair quality

education and promotion of the possibility to study

during all life for all;

5) provision of gender equality, empowering of all

women and girls;

6) provision of accessibility and stable water

resources and sanitation management;

7) provision of access to the low-cost, reliable,

stable and modern energy sources for everyone;

8) promotion of the progressive, integral and

sustainable economic growth, full and productive

employment and decent work for everyone;

9) creation of stable infrastructure, promotion of

the integral and stable industrialization and

innovations;

10) reduction of inequality;

Internal Audit of the Business Partner’s Reliability for Sustainable Development of the Enterprise

157

11) provision of openness, safety, vital capacity

and ecological sustainability of cities and other

settlements;

12) ensuring of the transfer to the rational patterns

of consumption and production;

13) application of urgent measures regarding the

fight with the change of the climate and its

consequences;

14) Conserve and sustainably use of the oceans,

seas and marine resources;

15) protection and restoration of terrestrial

ecosystems and promotion of their rational use, forest

conservation, desertification and stopping the process

of biodiversity loss;

16) assistance in building a peaceful and open

society in the interests of sustainable development,

ensuring access to justice for everyone and creating

effective institutions at all levels;

17) Revitalize the global partnership for

sustainable development (Decree of the President of

Ukraine, 2019).

According to the data of «Sustainable

Development Report 2021: The Decade of Action for

the Sustainable Development Goals» (UN et al.,

2021), prepared by the UN together with the

Bertelsmann Foundation and the University of

Cambridge, Ukraine ranked the 36 place in the world

ranking on the sustainable development index among

193 UN member states.

The following countries topped the top ten of the

global ranking on the Sustainable Development Index

in 2021: Finland (85,90), Sweden (85,61), Denmark

(84,86), Germany (82,48), Belgium (82,19), Austria

(82,08), Norway (81,98), France (81,67), Slovenia

(81,60), Estonia (81,58).

The Index of Sustainable Development (ISD) of

Ukraine according to the global assessment of the

progress of countries in achieving of the GSD was

75,51. The specified indicator characterizes the

general percent of the Ukrainian progress towards

achieving all 17 GSD. Over the past 20 years, the

dynamics of the Sustainable Development Index of

Ukraine characterizes a positive growth trend. The

Sustainable Development Index of Ukraine increased

from 71,47 in 2000 to 75,51 in 2021, an increase was

4,04.

The rate of assessment of side effects in Ukraine

in 2021 was 94%. The actual size of this assessment

indicates that Ukraine causes more positive and less

negative impacts on the ability of other countries to

achieve the GSD.

In order to analyze the actual state of achievement

17 of GSD of Ukraine in 2021, guiding by the ISD

analytics of Ukraine for the year 2021, it is rational to

emphasize the following groups of GSD.

Group 1: achieved or in the way of achievement

of GSD. Such goals include the GSD 1 “Without

poverty” and the GSD 10 “Reduction of inequality”.

Group 2: GSD, the problems of which remain

unresolved. This group includes: GSD 4 “Quality

education”, GSD 7 “Available and clean energy”,

GSD 12 “Responsible consumption and production”,

GSD 17 “Partnership for the sustainable

development”.

Group 3: GSD, the significant problems of which

are unresolved. This group includes: GSD 2

“Overcoming hunger, agricultural development”,

GSD 3 “Strong health and well-being”, GSD 5

“Gender equality”, GSD 6 “Clean water and Good

Sanitation”, GSD 8 “Decent Work and Economic

Growth”, GSD 9 “Industry, innovations and

infrastructure”, GSD 11 “Sustainable development of

cities and communities”, GSD 13 “Mitigation of

climate change”.

Group 4: GSD, the main problems of which

remain unresolved. The problematic goals of this

group include: GSD 14 “Life under the water”, GSD

15 “Life on the earth”, GSD 16 “Peace, justice and

strong institutions”.

This tendency of sustainable development of

Ukraine indicates a noticeable progress in the

development of the state in terms of its economy,

society and ecology. Over the past 20 years, Ukraine

has maintained its position at a level that is not lower

than the previously achieved GSD indicators.

However, the speed of achieving the GSD in Ukraine

remains low, and the availability of unsolved

problems with the peace, justice, institutions, decent

work, industry, innovations and infrastructure

requires an urgent response, both at the state level and

at the level of the individual enterprise.

The comprehensive achievement of the GSD of

Ukraine in 2030 requires the implementation of the

concept of sustainable development at the level of an

individual enterprise. The GSD of Ukraine should

become guidelines for the strategic planning of

domestic enterprises, since the balance of economic,

social and environmental dimensions of the

sustainable development of the state depends on the

results of each enterprise.

2.2 Business Partner’s Reliability of

Enterprise

Each enterprise can make a difference in different

way in the achievement of the state’s GSD. For

example: apply resource-saving technologies, reduce

ISC SAI 2022 - V International Scientific Congress SOCIETY OF AMBIENT INTELLIGENCE

158

the amount of harmful emissions, recycle wastes, pay

fair wages, participate in social projects (overcoming

hunger, development of sport, available education,

nature saving and other), counteract corruption and

fraud, pay taxes and fees, etc.

Achievement of the systemic effect of sustainable

development of the state is possible only when the

enterprise interacts with business partners, who

support the concept of sustainable development. The

mentioned development is an objective necessity for

enterprises, as they are all interested in a stable

environment for their own business, in which it

operates today and will function in the near future.

This means that the business partners of the enterprise

must carry out their economic activities in

compliance with the following principles of the

sustainable development: protection of human rights,

supremacy of law, involvement of the society,

corporate social responsibility, public-private

partnerships, nature conservation, innovative

technologies and other. The main condition for the

implementation of the listed principles of sustainable

development for the business partners of the

enterprise is reliability.

The reliability of a business partner of an

enterprise is a set of ethical determined by law

principles and rules, which should be followed by the

top management of enterprises in carrying out their

own economic activities in order to achieve the GSD

of a state.

According to the definition of reliability of a

business partner of an enterprise, a list of basic ethical

and legal norms should be provided and it compose a

culture of reliability in business.

The ethical norms of business are intended to

preserve the moral aspect of respect for universal

values, state symbols, patriotism, culture, national

traditions, history, human tragedies, religion, races,

and other.

It is advisable to assume it to the basic ethical

standards of the business partner’s reliability:

honesty; image; respect for property; legality; respect

for human rights; preservation of ecology;

responsibility to the state and society; counteraction

to corruption, fraud and other offenses. The specific

feature of the ethical norms of business is in the fact

that they are not supplied with the means of state

coercion. The state does not keep a systematic record

of violations of these norms of a business partner.

Moreover, information about a business partner's

ethics violation persists for a long time in the history

of media reports, social networks and people's

memory.

As for the laws that must be observed by the

business partners of the enterprise, they include

absolutely all current regulatory legal acts of the state,

which are applied to the scope of activities of

enterprises.

It should be noted that violation by a business

partner’s reliability in the field of economic activity

entails liability provided for by the norms of criminal,

administrative, tax, labour and other legislation of

Ukraine.

Violation of the business partner’s reliability is

shown in the form of certain legal actions, behaviour

or public statements of their owners, senior

management or personnel, which find their negative

assessment from the public society and competent

government authorities.

The Criminal Code of Ukraine No. 2341-III dated

April 05, 2001 (Criminal Code of Ukraine, 2001),

(hereinafter referred to as the CCU) defines a list of

the main types of offenses in the area of economic

activity, for which punishment is provided, namely:

- contraband (art. 201 of CCU);

- illegal production, storage, sale or transportation

excisable goods for the purpose of sale (art. 204 of

CCU);

- tampering of documents that are submitted for

the state registration of legal entities and sole

proprietors (art. 2051 of CCU);

- unlawful seizure of the property of an enterprise,

institution, organization (art. 2062 of CCU);

- legalization (laundering) of property, obtained

by criminal way (art. 209 of CCU);

- avoidance of payment of taxes, fees (mandatory

payments) (art. 212 of CCU);

- fraud with financial resources (art. 222 of CCU).

2.3 Area of Sustainable Development of

Enterprise in Ukraine

According to the data of the General Prosecutor's

Office of Ukraine, which are reflected in the annual

reports (“Unified Report on Criminal Offenses”) for

the period from 2017 to 2021 (General Public

Prosecutor’s Office of Ukraine, 2021), the total

number of offenses, committed by dishonest

enterprises in the area of economic activity of

Ukraine was: 5308 (2021), 5342 (2020), 5947 (2019),

6334 (2018) and 6297 (2017).

Of the total number of these offenses, it is

reasonable to emphasize the following types of them

(Table 1):

Internal Audit of the Business Partner’s Reliability for Sustainable Development of the Enterprise

159

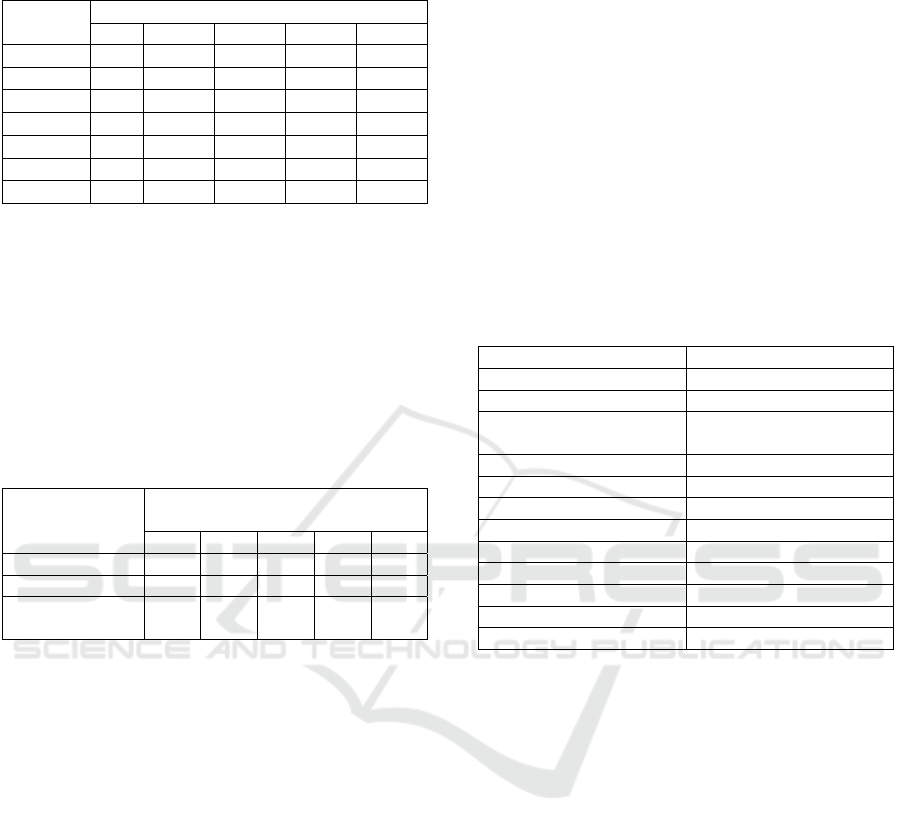

Table 1: Offences in the area of business activity in Ukraine

for the period from 2017 - 2021.

Articles of

the CCU

Total number of offences, items.

2017 2018 2019 2020 2021

Art. 201 102 125 112 114 124

Art. 204 596 574 562 615 603

Art. 205

1

292 269 478 635 416

Art. 206

2

82 70 130 90 76

Art. 209 243 242 283 348 360

Art. 212 1009 1099 852 910 746

Art. 222 61 58 76 142 146

According to the data of the General Prosecutor's

Office of Ukraine (General Public Prosecutor’s

Office of Ukraine, 2021), the main reasons of

material losses due to violation, by the dishonest

enterprises, in the area of business activity were non-

payment of taxes and fees, reception of unlawful

benefit and arrest of a property. The detailed

information is presented in Table 2.

Table 2: Losses due to offences in the area of business

activity in Ukraine for the period from 2017 - 2021.

Indicator

Losses due to offences,

millions of UAH.

2017 2018 2019 2020 2021

Unpaid taxes 3285 1254 1261 1252 2346

Unlawful benefit 55 207 34 73 392

Arrest for a

p

ropert

y

4770 2917 7584 5700 5356

Analysis of quantitative (Table 1) and cost (Table

2) indicators of violations by dishonest enterprises in

the area of business activity of Ukraine allows us to

make the following conclusions:

a) the biggest number of offenses falls on

avoidance of payment of taxes, illegal transactions

with excisable goods and tampering of documents for

business registration;

b) the tendency of a long-durable increase in the

number of violations is observed in contraband, fraud

with financial resources, illegal transactions with

excisable goods, tampering of documents for business

registration, legalization of property obtained by

criminal means;

c) there is a long-term activity of offenses by

dishonest enterprises in the area of business.

It is advisable to continue a systematic study of

the business partner’s reliability in the field of

business activity of Ukraine by analyzing the relevant

indices, ratings and assessments, carried out by

international organizations in the area of economics,

ecology and society.

According to the Index of Economic Freedom

(IEF), Ukraine in 2021 took the 127 th place out of

184 countries of the world and the last place among

45 countries of the European region. The assessment

of Ukraine's economic freedom is 56,2 (0 = worst,

100 = best), which is 1.3 points more than in 2020

(54,9). The total rate of Ukraine is below regional

(70,1) and world (61,6) average indicators. Such data

is published in the annual manual “The Index of

Economic Freedom 2021” (Index of Economic

Freedom, 2021) by the analytic centre No. 1 “The

Heritage Foundation” in Washington. The detailed

information on the constituent components of the

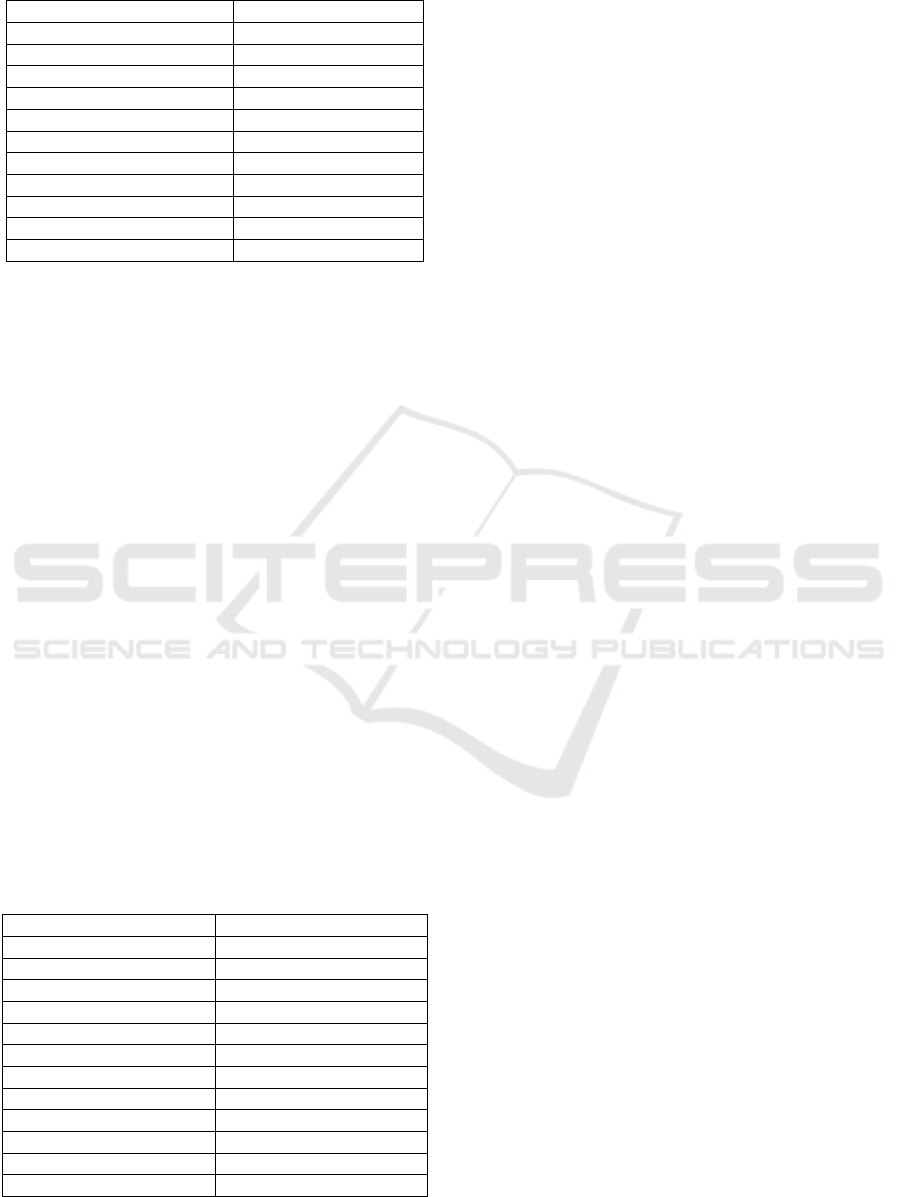

IEF, - 12 economic freedoms, shown in Table 3.

Table 3: The assessment of the components of IEF of

Ukraine in 2021.

IEF com

p

onents Evaluation, ratin

g

Right of property 48,5

Judicial efficac

y

41,1

Honesty of the

g

overnment

37,9

Tax loading 88,7

State expenses 48,2

Fiscal health 87,7

Business freedom 63,5

Labor freedo

m

48,7

Monetary freedom 65,8

Trade freedo

m

79,2

Investments freedom 35,0

Financial freedom 30,0

The data, presented in Table 3 regarding the

economic freedoms of Ukraine indicates the

underdevelopment of the economic system, which

cannot fully ensure the freedom of entrepreneurship,

the movement of capital, investment, labour,

production, consumption, government honesty, and

other. The low level of economic freedoms in Ukraine

has a negative impact on the observance of reliability

by enterprises.

The Environmental Performance Index (EPI) of

Ukraine in 2020 was 49,5 (0 = worst, 100 = best). The

presented estimation puts Ukraine in the 60 th place

out of 180 countries in the EPI rating. The ten-year

dynamics of EPI for Ukraine is 0,7 (Environmental

Performance Index, 2020). EPI determines the level

of environmental health and ecosystem vitality within

a state. To evaluate the degree of achievement of

individual environmental policy goals of Ukraine, it

is advisable to consider the components of the EPI

(Table 4).

ISC SAI 2022 - V International Scientific Congress SOCIETY OF AMBIENT INTELLIGENCE

160

Table 4: Estimation of the EPI components of Ukraine

2020.

EPI components Estimation, rating

Ai

r

qualit

y

39,8

Sanitation, drinking wate

r

55,1

Heav

y

metals 69,3

Waste mana

g

ement 73,1

Biodiversit

y

37,7

Ecosystem Services 30,2

Fishing 12,4

Change of climate 69,2

Pollution emissions 76,6

A

g

riculture 79,5

Water resources 14,1

The EPI component evaluation indicates that

Ukraine has significant environmental problems with

fisheries, water resources, lack of ecosystem services,

biodiversity, air quality, etc. The overall EPI value

shows that the environmental problems, faced by

Ukraine are solved in the current period by 50 %. To

achieve environmental progress, it is necessary to

clarify the environmental policy of the state and to

attract significant investments in “green

technologies” of enterprises. The presence of

unresolved environmental problems and the necessity

for additional investment in their solution indicate

that enterprises are not observing the reliability.

According to the data of the World Economic

Forum, provided in 2019 Global Competitiveness

Report (Global Competitiveness Report, 2019), the

Global Competitiveness Index (GCI) for Ukraine in

2019 was 57 (0 = worst, 100 = best), what allowed it

to take the 85th place in the rating among 141

countries of the world. The value of this index

characterizes the economic prosperity in Ukraine,

which in fact, corresponds to the level 2/3 of the

possible. The detailed information on the evaluation

of GCI components is given in Table 5.

Table 5: Evaluation of the GCI components of Ukraine in

2019.

GCI com

p

onents Evaluation, ratin

g

Institutions 47,9

Infrastructure 70,3

ICT adoption 51,9

Macroeconomic stabilit

y

57,9

Health 65,6

Skills 69,9

Product market 56,5

Labor market 61,4

Financial syste

m

42,3

Market size 63,0

Business d

y

namism 57,2

Innovation ca

p

abilit

y

40,1

According to the evaluations, given in Table 5, the

main reasons for the low level of competitiveness of

the national enterprises are low innovation ability,

passivity of society, a high level of organized crimes,

low qualifications of the personnel, ineffectiveness of

the state institutions, problems in the financial

system, macroeconomic instability, etc. Accordingly,

a big competitiveness provokes the national

enterprises to violate the reliability.

The analysis of the facts of offenses by dishonest

enterprises in the area of business activity of Ukraine,

its global trends in economic freedom, environmental

efficiency and socio-economic competitiveness

allows us to conclude that the reliability of the

national business is in an unfavourable and aggressive

environment. This means that the enterprise has a

high probability to become a victim of a dishonest

business-partner.

In order to achieve the reliability of its own

business, an enterprise is forced to pay significant

attention to the business partner’s reliability in its

external supply chains. The mentioned attention

should be expressed in the form of monitoring of the

risks from interaction with dishonest business

partners and the ability to respond quickly to the

potential threats to the sustainable development of the

enterprise. This need is due to the fact that state

institutions and public opinion are interested not only

in the reliability of the enterprise, but are largely

interested in its business partners, therefore the issue

of the business partner’s reliability is also very

important.

2.4 Risks of Dishonesty of Business

Partners for Enterprise

The violation of the business partner’s reliability of

an enterprise, as of the second side of economic legal

relations, is potentially capable to cause a real damage

to its sustainable development. In order to gain a

deeper understanding of the essence of the problem,

it is advisable to consider in detail the main types of

its risks and to show the potential consequences

(harm) for an enterprise.

Risk No.1: public statements by the top

management of a business partner or its owner in the

mass media or social networks about support for the

occupation, aggressor countries, illegal armed

groups; discrimination against the state symbols

(flag, coat of arms, anthem), language, culture and

history; racial intolerance; violation of human rights

and other. The consequences for the enterprise: public

condemnation on the part of citizens (buyers) and

enterprises (contractors), which is expressed in the

Internal Audit of the Business Partner’s Reliability for Sustainable Development of the Enterprise

161

deliberate refusal to purchase its goods or services;

termination of agreements; supply interruptions;

damages; decrease of the company's securities,

quoted on the stock exchanges, etc.

Risk No.2: a corruption scandal with the

involvement of a business partner’s representatives.

Consequences for the enterprise: involvement of

senior management in public scandals; additional

checks by regulatory authorities; damage to business

reputation; suspension of contracts execution and

other.

Risk No.3: inclusion of a business partner in the

"lists of sanctions" of the UN Security Council, the

USA, the European Union, the United Kingdom,

Ukraine and other states. The consequences for the

enterprise: arrest of assets; prohibition to the owners

and senior management from entering certain states;

the prohibition of trade at the regional markets;

banking restrictions on obtaining loans and

conduction of other financial transactions; a ban on

transactions with shares and debt instruments; a ban

to make the production and other economic activities.

Risk No.4: implementation of fictitious business

transactions by a business partner. Consequences for

the enterprise: loss of value added tax credit; illegal

overstatement of costs during calculation of the

financial result; court cases; fines; damages; criminal

responsibility.

Risk No.5: conflicts between the top management

of a business partner with the workforce and trade

union organizations. Consequences for the enterprise:

workers' solidarity strike; unplanned inspections of

the regulatory authorities; journalistic investigations;

damage to the image; staff turnover among senior

management and leading specialists; bad reputation

of the company at the labor market.

Risk No.6: contamination of the environment by

a business partner. Consequences for the enterprise:

scandal with violation of environmental safety at the

place of production and in the region; lawsuits from

injured workers and citizens; compensation to

victims; additional checks by regulatory authorities;

fines; stop of production; disruption of delivery

timeliness and other.

Risk No.7: The business partner meets the criteria

for a shell company that launders illegal funds

(evasion of the payment of taxes, corruption, other

financial crimes) and finances terrorism.

Consequences for the enterprise: blocking of funds on

current accounts by subjects of the financial

monitoring; loss of funds (advances) or goods after

their transfer to a business partner; unscheduled

inspections by regulatory authorities; litigation;

additional expenses; criminal liability of top

management and other.

Risk No.8: the business partner, registered in

offshore. Consequences for the enterprise: violation

of transfer pricing legislation; judicial disputes;

additional expenses; non-fulfilment of agreements;

loss of assets (advance payment or goods) and other.

Risk No.9: violation of customs regulations by a

business partner and contraband. Consequences for

the enterprise: termination of the supply chain;

disruption of supplies and loss of time to find and

replace a counterparty; shutdown of production;

additional losses; damage.

Risk No.10: limited access to information on

beneficial ownership and key persons of the business

partner. Consequences for the enterprise:

vulnerability of entry to the business of organized

crime groups or terrorist organizations, using

complex forms of corporate structures; judicial

disputes; additional expenses.

Risk No.11: a close relationship between a

business partner and political parties or politicians.

Consequences for the enterprise: political pressure on

the enterprise with the help of state regulatory bodies;

unreliability of a business-partner, when changing

political forces in the state.

Risk No.12: hiding of financial problems in the

financial statements of a business partner.

Consequences for the enterprise: there is a high

probability of bankruptcy of the business partner; loss

of assets (advances or goods); interruptions in

production, supply, payment of receivables paid and

other.

The abovementioned list of risks of violation of

the business partner’s reliability can cause significant

financial losses to the enterprise, create problems

with the law, the public and the counterparties, and

most importantly, cause the termination of its

business activities. However, a timely avoidance of

interaction with a non-virtuous business partner

allows an enterprise to achieve positive results in its

work, namely: stability and reliability of the

enterprise's business processes in the long term

perspective; reliable reputation and significant

customer loyalty at the market; absence of problems

with the law; avoidance of unproductive expenses;

financial stability; profitability; attractiveness for

talented employees; helps to attract investments;

introduction of resource-saving technologies; eco-

friendly products; social projects; the success story of

a reliable partnership and etc.

Based on the above threats and the perspectives

for their absence, the enterprise needs to work out its

own model of prudence, which will ensure that safe

ISC SAI 2022 - V International Scientific Congress SOCIETY OF AMBIENT INTELLIGENCE

162

management decisions are made on choosing a new

business partner or continuing or terminating of

cooperation with an existing business partner. The

purpose of this model should be a deep understanding

of the risks from the ways of doing business by a

business partner, reception of the control and

analytical information about the facts of violations of

the business partner’s reliability and avoidance of

cooperation with a problematic business partner.

2.5 Improvement of the Internal Audit

Method

For the practical implementation of the idea of

prudence in the work with the business partners at the

enterprise, it is advisable to create an internal audit

unit, one of the main functions of which will be the

monitoring of the risks of violation of the business

partner’s reliability. The advantage of internal audit

over the ability to involve external audit is that such

control will be carried out on an ongoing basis.

The effectiveness of internal audit in combating

the risks of dysfunctional business partners requires

proactive loans, rapid processing of large amounts of

information, the use of innovative methods of

searching for information on the Internet, a high level

of awareness of auditors about legislation (criminal,

tax, environmental, informational, administrative,

and etc.) and moral and ethical standards in the

society, critical thinking of auditors, rapid collection

of evidences, development of proposals for solutions

to avoid or minimize existing risks.

The traditional methodology of internal audit as a

subject of control over the risks of dishonesty of

business partners requires the addition of the

following provisions:

1) about the object of internal audit, - the virtue of

business partners in execution of their own economic

activities, which can have the following risks:

scandalous statements, corruption, international

sanctions, fictitious business transactions, conflict

with the workforce, environmental pollution, shell

companies, offshore companies, contrabands,

harboring of the beneficiary, political dependence and

inaccurate financial statements. This list of risks is not

exhaustive and may contain other risks depending on

the specifics of the business partner's activities.

2) about the information sources of internal audit.

The main feature of conduction of an internal audit of

the risks of a business partner's dishonesty is

complete distance - verification of reliability is

carried out without personal contact with a business

partner, without access to his internal documentation,

without communication with his staff, without

acquaintance with his technologies, etc. The business

partner does not need to know that the company is

checking him. In modern conditions of the

development of a digital society, to collect

information about the reliability of a business partner,

it is advisable for internal audit to use information

from open sources, namely:

- open state registers and databases on business

registration, tax information, licensing, permits,

inspections of the state bodies, registered property,

court decisions, legal actions, etc. For example: "The

Unified State Register of Legal Entities, Individual

Entrepreneurs and Public Organizations"; “Learn

more about the partner's business from DFSU”;

"Unified License Register"; "State Register of Rights

to Real Estate"; "Cadastral Map of Ukraine";

"Unified state register of the Ministry of Internal

Affairs for registration of vehicles"; "Unified State

Register of Court Decisions"; "Information about

bankruptcy cases"; "Unified state register of persons

who have committed corruption offenses";

- mass media (television, radio, press, internet,

etc.);

- social networks (Facebook, Twitter, Instagram,

YouTube, web forums, etc.);

- other sources (private databases of

counterparties, reviews or interviews about a business

partner from laid-off workers, etc.).

3) about special methods of information tracking

on the Internet. In the modern conditions of the

information society, the search of information about

the facts of violations of a business partner’s

reliability requires the study of large amount of

information in cyberspace, therefore, internal audit

must use informational search systems. These

systems allow you to collect the necessary

information, process it according to certain criteria

and save it in a user-friendly format. The

disadvantage of traditional search systems is that

much of the information on the Internet and local

databases is practically inaccessible. The reason for

this is that the search algorithm uses only the keyword

matching criterion and completely ignores the

semantic meaning of the words, that is, the context of

the search query. One of the perspective ways to

collect information about the reliability of a business

partner of an enterprise is to develop its own semantic

search system on the Internet. Such a search system

operates with the use of data on the structural

elements of the search object, its properties and

relation with other information objects. The

individuality of this system lies in the uniqueness of

the search algorithm, which takes into account the

content of words in the search query. Such approach

Internal Audit of the Business Partner’s Reliability for Sustainable Development of the Enterprise

163

concentrates the search in the meaning of keywords

instead of the traditional search for their matches.

Semantic search is able to provide an internal audit

not only of information about the sites on which the

keyword was found on the request, but also specific

information corresponding to the essence of the

search request. The practical application of the

semantic search system at the enterprise requires its

development with the help of involved programmers

and an individual technical task of internal audit. An

example of such tasks can be the search for

information about a business partner in the context of

court decisions (decisions or judgments),

enforcement proceedings, content of owners or top

management in social networks, tax debts, founders

and the size of the authorized capital, codes of the

type of economic activity (СTЕА), related

counterparties through single directors (in parallel),

being in the process of termination, financial state,

media analysis, availability of licenses and permits,

etc. The main indicators of the effectiveness of the

search system for the needs of internal audit should

be relevance, completeness of the base, taking into

account of the semantics of the keywords of the

query. The typical examples of such programs are:

«Kngine», «Hakia», «Kosmix», «DuckDuckGo»,

«Evri» and other.

4) about a critical analysis of the risks of

dishonesty of a business partner. It is advisable to

analyze the selected information about a business

partner exclusively through the critical thinking of

internal auditors. Therefore, internal auditors must

meet a high level of practical awareness of potential

issues from a business partner in the moral and legal

environment of business implementation. The

identified risks of dishonesty for a business partner

must necessarily be based on the verified evidences.

Therefore, the information, obtained from the results

of the search system’s work, with the exception of

information, obtained from open state registers or

databases, requires additional verification at the level

of the primary source (review of facts, familiarization

with the original documents, communication with

witnesses or participants of the events).

5) about informational support for confident

management decisions for cooperation with a

business partner. The practical result of the work of

internal audit is control and analytical information

about the business partner, which in an available form

discloses to the top management the following:

- characteristics of the business partner, its owner

and top management;

- existing risks of trouble for a business partner;

- evaluation of potential damage to the enterprise;

- a recommendation for cooperation with a

business partner.

Depending on the level of evaluation of potential

damage, the internal audit may recommend, not

recommend, or not deeply recommend the

cooperation of the enterprise with a specific business

partner. Also, the internal auditor can recommend

measures to minimize existing risks, namely: 100 %

advance payment, additional terms of business

agreements on compensation and fines for damage

caused to the company, surety and guarantees.

However, the final decision on cooperation with the

business partner is made by the top management of

the enterprise.

The abovementioned proposals for improvement

of the traditional methods of internal audit should be

reflected in the internal documents of the enterprise.

For this, it is advisable at the enterprise to issue the

Regulation “On the internal audit of the reliability of

a business partner”. This document must be

developed by the head of the internal audit

department and approved by the director of the

enterprise. Based on this provision, the internal audit

department develops job (work) instructions for

auditors that are directly involved in the internal audit

procedures for the reliability of a business partner.

It should be noted that the control and analytical

information about the dishonesty of a business partner

is intended only for the owners and senior

management of the enterprise, therefore, access to

such information for other employees should be

limited.

3 CONCLUSIONS

At the beginning of the XXI century, Ukraine has

joined the process of globalization of the world’s

sustainable development and has committed itself to

fulfil 17 SDGs by 2030. Achieving these goals

requires the creation of appropriate conditions for

sustainable development of the enterprise, which will

allow its management to balance economic,

environmental and social factors of business activity.

The actual indicators of Ukraine’s implementation of

the SDGs, economic freedoms, environmental

efficiency, global competitiveness and crime rate in

the field of economic activity together show that the

state does not pay enough attention to the conditions

for sustainable development of the enterprise.

The responsibility for the sustainable

development of domestic enterprises is rested on their

owners and senior management. Achieving

sustainable development of the enterprise in an

ISC SAI 2022 - V International Scientific Congress SOCIETY OF AMBIENT INTELLIGENCE

164

unfavourable and aggressive environment requires

management to exercise some caution to work with

honest business partners.

The honesty of the enterprise’s business partner

should be understood as a set of ethical principles and

rules set by law, which should be ruled by the top

management of enterprises when carrying out their

own business activities in order to achieve the SDGs

of the state.

The main risks of the honesty breaching by

business partners include: scandalous statements,

corruption, international sanctions, fictitious business

actions, conflict with the workforce, environmental

pollution, shell corporations, offshore, smuggling,

concealment of beneficiaries, political dependence,

financial inaccuracy and others.

If the enterprise interacts with an unfair business

partner it can cause problems (harm), such as

additional inspections of regulatory authorities,

litigation, unproductive costs, fines, reputational

losses, environmental pollution, public conflicts,

corruption scandals and others.

In order to increase the effectiveness of the

enterprise’s struggle against the risks of dishonesty of

business partners, the traditional method of internal

audit requires some improvements in the following

provisions:

internal audit object - the honesty of business

partners in carrying out their own business activities

with its inherent risks of corruption, international

sanctions, fictitious business actions, conflict with the

workforce, environmental pollution and others;

information sources of internal audit include open

state registers and databases, mass media, social

networks and other sources;

the internal audit usage of special software

products for searching the Internet, which operate on

the principles of the semantic search system;

critical analysis of risks of business partner

unfairness;

information support for confident management

decisions on cooperation with an honest business

partner.

Thus, the internal audit of the honesty of business

partners at the enterprise allows its management to

achieve the appropriate level of deliberation in

choosing safe business partners. This approach

effectively contributes to the sustainable

development of the enterprise in the long-term

outlook.

REFERENCES

Abbas, D. S., Ismail, T., Taqi, M., Yazid, H. (2021). The

influence of independent commissioners, audit

committee and company size on the integrity of

financial statements. Estudios de Economia Aplicada

39 (10).

Bondarenko, T., Dutchak, R., Kondratiuk, O., Rudenko, O.,

Shaikan, A., Shubenko, E. (2020). Internal Audit of

Conflicts in Enterprise’s Accounting with the Help of

Artificial Intellect’s Instruments. Atlantis Press 129, p.

39-46.

Criminal Code of Ukraine No. 2341-III dated 5.04.2001.

De Capitani Di Vimercati, S., Foresti, S., Paraboschi, S.,

Samarati, P. (2020). Enforcing corporate governance's

internal controls and audit in the cloud. IEEE

International Conference on Cloud Computing,

CLOUD 2020-October, 9284333, p. 453-461.

Decree of the President of Ukraine “On the goals of

sustainable development of Ukraine for the period up to

2030” No.722/2019 dated September 30, 2019.

Dutchak, R., Kondratiuk, O., Rudenko, O., Shaikan, A.

Shubenko, E. (2021). Internal Audit of Cybercrimes in

Information Technologies of Enterprises Accounting.

SHS Web of Conferences 100, 01006 (2021).

General Public Prosecutor’s Office of Ukraine. (2021).

https://old.gp.gov.ua/ua/statinfo.html.

Handayani, S., Kawedar, W. (2021). Could the

minimization of opportunity prevent fraud? An

empirical study in the auditors’ perspective.

Accounting 7(5), p. 1157-1166.

Khersiat, O. M. (2020). The efficiency of applying the

internal control components based on COSO

framework to transparently carry out tasks and services,

ensure integrity and enhance quality and efficiency:

Case study-the greater amman municipality.

International Journal of Financial Research 11(2), p.

371-381.

Korkushko, O. N., Kushnir, L. А. (2020). Internal audit at

the enterprise: essence and specific features of

organization. Infrastructure of the market 42, p. 363-

366.

Mocanu, M., Ciurea, C. (2019). Developing an index score

for the internal auditor profile in Romania based on real

data analysis. Economic Computation and Economic

Cybernetics Studies and Research 53 (2), p. 93-111.

Rahahleh, M. H., Hamzah, A. H. B., Rashid, N. (2021). The

Artificial Intelligence in the Audit on Reliability of

Accounting Information and Earnings Manipulation

Detection. Studies in Computational Intelligence 974,

p. 315-323.

Raji, I. D., Smart, A., White, R. N., (...), Theron, D., Barnes,

P. (2020). Closing the AI accountability gap: Defining

an end-to-end framework for internal algorithmic

auditing. FAT* 2020 - Proceedings of the 2020

Conference on Fairness, Accountability, and

Transparency, p. 33-44.

Resolution 70/1 of the UN General Assembly

“Transformation of our world: the 2030 Agenda for

Sustainable Development” dated September 25, 2015.

Internal Audit of the Business Partner’s Reliability for Sustainable Development of the Enterprise

165

Salagrama, S. (2021). An Effective Design of Model for

Information Security Requirement Assessment.

International Journal of Advanced Computer Science

and Applications 12 (10), p. 1-5.

Sustainable Development Report 2021: The Decade of

Action for the Sustainable Development Goals. (2021).

https://dashboards.sdgindex.org.

The 2020 Environmental Performance Index. (2020).

https://www.epi.yale.edu.

The Global Competitiveness Report 2019. (2019).

https://www.weforum.org/reports?year=2019#filter.

The 2021 Index of Economic Freedom. (2021).

https://www.heritage.org/index/country/ukraine.

Turker, I., Bicer, A. A. (2020). How to Use Blockchain

Effectively in Auditing and Assurance Services.

Contributions to Management Science, p. 457-471.

ISC SAI 2022 - V International Scientific Congress SOCIETY OF AMBIENT INTELLIGENCE

166