The Effect of Service Innovation and Self Service Technology on

Customer Satisfaction PT Bank Negara Indonesia (Persero) Tbk Kc

Medan

Mufida Sari

Master of Management Science, Faculty of Economics and Business, University of North Sumatra, Medan, Indonesia

Keywords: Service Innovation, Self Service Technology, E-Satisfaction.

Abstract: This study aims to identify and analyze service innovation and self service technology on e-satisfaction at PT

Bank Negara Indonesia (Persero) Tbk during February to April 2022. Currently, the banking industry is

competing to develop technology-based products and services. In order to compete, survive, and thrive, the

banking industry must make new innovations to provide convenience to customers in meeting customer needs.

Innovation in the banking industry can be done by adopting various self service technologies (SST). Service

innovations such as service concept, customer interface, service development and delivery, and technological

options are taken into consideration in measuring customer satisfaction. Self service technology such as

functionality, enjoyment, security/privacy, design, convenience, customization, and assurance are also

considered in measuring customer satisfaction. This research is a quantitative research with causal associative

research. The population in this study are customers of PT Bank Negara Indonesia (Persero) Tbl who have

used BNI mobile banking. The sampling technique used was random sampling so that there were 100

customers who were the samples in this study. The results showed that service innovation and self service

technology had a positive and significant effect on e-satisfaction.

1 INTRODUCTION

Technological developments affect companies in

carrying out their functions in order to survive in the

current market. The invention of increasingly

sophisticated technology is intended to provide

positive benefits for life while simplifying human

work. Almost all daily human activities are supported

by this technology, not least in running the business

that occurs in the company, including in the banking

sector. Currently, the banking industry is competing

to develop both technology-based products and

services . In order to compete, survive, and thrive, the

banking industry must make new innovations to

provide convenience to customers in meeting

customer needs. This is in line with what Lovelock

(2012) stated that the service sector is the sector that

experiences the biggest changes due to the rapid

changes experienced by other factors such as

technological changes which directly increase the

competitive climate in the banking industry.

The banking industry needs to innovate in

combining digital technology with customer

interaction, in this case the findings of these new

technologies must make it easier and provide

convenience for customers in accessing banking

services. According to Kotler & Keller (2009)

innovation is related to new things that are created as

a form of breakthrough to products, services, ideas,

and perceptions from someone which can be in the

form of new products, development of new products,

design changes, technical innovations, and so on. new

business ideas or new processes. Innovation in the

banking industry can be done by adopting various

kinds of self service technologies (SST) (Orel and

Kara, 2013). Meuter et al (2000) define self service

technologies as technological interfaces that allow

consumers to produce a service independently of the

direct involvement of company employees. Self

service technologies are expected to provide

customer satisfaction through information

technology-based services such as performance,

information, security and sensation in using e-

banking.

According to Kotler and Keller (2009)

satisfaction is a person's feelings of pleasure or

Sari, M.

The Effect of Service Innovation and Self Service Technology on Customer Satisfaction PT Bank Negara Indonesia (Persero) Tbk Kc Medan.

DOI: 10.5220/0011823100003460

In Proceedings of the 4th International Conference on Social and Political Development (ICOSOP 2022) - Human Security and Agile Government, pages 383-390

ISBN: 978-989-758-618-7; ISSN: 2975-8300

Copyright

c

2023 by SCITEPRESS – Science and Technology Publications, Lda. Under CC license (CC BY-NC-ND 4.0)

383

disappointment arising from comparing the perceived

performance of the product (or outcome) against their

expectations.

The digitalization trend that demands speed and

convenience makes PT Bank Negara Indonesia

(Persero) Tbk continue to innovate to meet the needs

of its customers. Especially in services through self-

service technology which is expected to be easier,

faster, and more reliable to use in transactions. In

order to meet the different needs of each customer, PT

Bank Negara Indonesia (Persero) Tbk always makes

efforts to improve customer mobile banking

transactions . The following is a table of BNI mobile

banking users from January to March 2022 in Medan

City.

Table 1: Number of BNI Mobile Banking Users in Medan

City January – March 2022.

Month Number of Users

January 83%

February 19%

March 63%

Source: https://trends.google.com.

Table 1. shows that BNI mobile banking users

from January to March 2022 in Medan City

fluctuated. This indicates customer.

Previous research conducted by Sakun Boon Itt

(2015) showed that self-service technology positively

affects e-satisfaction. Meanwhile, research by Evan

Setiawan (2016) reveals that self-service technology

leads to reduced interactions between company

employees and customers to create results from

services. According to McCollough in Evan Setiawan

(2016) the relationship between service failure and

customer satisfaction can be explained by looking at

initial disconfirmation and recovery disconfirmation .

Previous research on the effect of service innovation

on e-satisfaction was conducted by Rew (2020) which

showed that innovation in service companies

positively affects customer satisfaction. Research

conducted by Simon (2020) found that not all

dimensions of innovation affect satisfaction.

Based on the description above, in connection

with the importance of knowing the effect of service

innovation and self service technology in increasing

customer satisfaction, the authors are interested in

conducting research with the title:

"The Influence of Service Innovation and Self

Service Technology on Customer Satisfaction of PT

Bank Negara Indonesia (Persero) Tbk KC Medan".

2 LITERATURE REVIEW

2.1 Service Innovation

According to Drucker (2012), innovation is a specific

tool for companies where innovation can explore or

take advantage of changes that occur as an

opportunity to run a different business. Innovation is

related to new things that are created as a form of

breakthrough to products, services, ideas, and

perceptions from someone which can be in the form

of new products, development of new products,

design changes, technical innovations, to new

business ideas or new processes. (Kotler & Keller,

2009). According to (Delafrooz et al, 2013) service

innovation can make consumers very satisfied with

the services provided. With this innovation, there will

be continuous quality improvement so that consumers

will feel more satisfied and reluctant to switch to

other products or companies:

Hertog (2010) defines service innovation in a

four-dimensional model as follows:

1. Service Concept

Creation of new concepts in services in specific

markets.

2. Customer Interface

Refers to the process of interface interaction

between service providers and consumers because

this process is included in the process of creating

services and value. The interface can be face-to-

face, or through electronic media.

3. Service Development and Delivery

Service development and delivery. These

activities involve infrastructure, processes, and

employees to produce and deliver services to

consumers.

4. Technological Options

Choice of technology used, especially

information technology. This is important for

services because it allows for greater efficiency

and effectiveness.

2.2 Self Service Technology (SST)

The term "SST" was first used by Meuter et al (2000).

SST is defined as a technology interface that allows

consumers to produce a service independently from

the direct involvement of company employees.

Continuous progress from traditional service delivery

to modern SST is essential for all service industries.

Moreover, many customers turn to internet-based

services because they find it easy to use, fun, and

convenient (Meuter et al., 2000).

ICOSOP 2022 - International Conference on Social and Political Development 4

384

According to Hsieh et al (2006) there are seven

dimensions of self-service technology (SST) quality,

namely:

1. Functionality

This dimension represents the functional

characteristics of self-service technology (SST),

namely:

a. Reliability (reliability)

Is the power to provide guaranteed services

reliably and on target.

b. Responsiveness (responsiveness)

Is the ability of SST devices to respond to

commands entered into the system by

customers.

c. Simple and easy to use

Is the SST device can be operated easily and

requires little effort.

d. Respond to requests quickly

Is the service on the SST device can be

completed in a short time.

2. Enjoyment

It is the perception of pleasure and interest that the

user encounters while using and after using the

SST device.

3. Security/Privacy

Refers to freedom from risk or doubt that the user

will feel. The facilities provided by the SST

device in building a sense of security and comfort

for consumers in their operation.

4. Design

Covers the overall look of the SST, which gives it

a good aesthetic appearance. The beauty of the

shape and arrangement of the SST device to create

an attractive appearance for the user.

5. Assurance

Describing confidence because of the reputation

and competence of the SST device that prioritizes

trust because of the reputation and competence of

the SST provider. Assurance can create a sense of

security for its consumers.

6. Convenience Dimension of convenience

Describes the accessibility of SST services, with

the ease and convenience of SST services to use.

7. Customization

This is the dimension in which SST devices can

be changed to suit consumer preferences and

desires. Aims to understand and meet user needs

without being fixated on the structure of the

system.

2.3 E-Satisfaction

The word satisfaction comes from the Latin "satis"

(meaning good enough, adequate and "facio" to do or

make). Satisfaction, according to Oliver (1997) is "a

summary of the psychological states that result when

emotions around unconfirmed expectations are

combined with consumers' prior feelings about the

consumer experience." From his point of view,

"satisfaction is perhaps best understood as the

ongoing evaluation of the surprise inherent in the

product acquisition and/or consumption experience."

The dimensions of satisfaction by Hawkins and

Looney in Tjiptono (2011) are reviewed from 6

aspects as follows:

1. Overall Customer Satisfaction (Overall Customer

Satisfaction)

Considering the level of customer satisfaction of

the company's services and compare them with

competitors ' services as a whole.

2. Dimensions of Customer Satisfaction

By identifying the dimensions that are the core of

customer satisfaction based on specific items that

most influence overall customer satisfaction .

3. Conformance of Expectations (Confirmation of

Expectation)

Obtained on the basis of conformity or

discrepancy between customer expectations

regarding the quality of products or services from

the company.

4. Repurchase Intent (Repurchase Intent)

Customer satisfaction or not is obtained from

seeing whether there will be a repeat purchase of

a product from the same customer .

2. Willingness to Recommend (Willingness to

Recommend)

Here can be seen customer loyalty to promote

either directly or indirectly the company's services

to others.

3. Customer Dissatisfaction (Customer

Dissatisfaction)

Aims to re-examine what aspects of customer

dissatisfaction.

In this study, to evaluate customer satisfaction, the

indicators used according to Tjiptono (2014) are as

follows:

1. Conformance of expectations

2. Interest in visiting or repurchasing

3. Willingness to recommend

2.4 Relationship of Service Innovation

to E-Satisfaction

E-Satisfaction is a measuring tool for companies to

survive in a competitive market environment. In the

research of Rew, et al. (2020) explains that customer

satisfaction can be generated from the customer's

experience in using the service, besides the system

The Effect of Service Innovation and Self Service Technology on Customer Satisfaction PT Bank Negara Indonesia (Persero) Tbk Kc Medan

385

used by consumers in running the service can increase

consumer satisfaction. So with service innovation, it

can encourage customers to play an active role in the

service process. Innovation explicitly increases the

company's opportunities to meet very high customer

needs, so companies can easily create customer

satisfaction. In the banking sector, service innovation

measures the effectiveness provided to customers and

can create customer satisfaction and loyalty. Thus, the

hypotheses related to service innovation on e-

satisfaction are as follows:

H1: Service Innovation has a positive effect on E-

Satisfaction

2.5 Relationship of Self Service to

E- Satisfaction

Self service technology is defined as an interface

technology that allows consumers to produce a

service independently of the direct involvement of

company employees (Meuter et al, 2000). Sakun

Boon Itt's research (2015) shows that self-service

technology positively affects e-satisfaction. E-

Satisfaction comes from customer expectations, in

this case self service technology will meet customer

expectations in its service. Manual service sometimes

creates problems, given the inevitably long queues.

So it appears, there is a gap between expectations and

the reality of the service received by customers. Self

service technology actually fills this gap. Customers

who want fast and accurate service will greatly

benefit from responding to the application of

technology. So that self-service technology will have

a positive effect on e-satisfaction. So the hypothesis

related to self service technology on e-satisfaction is

as follows:

H2: Service Innovation has a positive effect on E-

Satisfaction

Service

Innovation

(X1)

Self service

technology

(X2)

Figure 1. Conceptual Framework.

3 RESEARCH METHOD

For the mutual benefit and protection of Authors and

Publishers, it is necessary that Authors provide

formal written Consent to Publish and Transfer of

Copyright before publication of the Book. The signed

Consent ensures that the publisher has the Author’s

authorization to publish the Contribution.

The copyright form is located on the authors’

reserved area.

The form should be completed and signed by one

author on behalf of all the other authors.

3.1 Types of Research

The type of research used in this study is causal which

aims to analyze how one variable affects other

variables. This study was to analyze the effect of

service innovation and self service technology on e-

satisfaction . This research was conducted at PT Bank

Negara Indonesia (Persero) Tbk starting from

February to April 2022.

3.2 Population and Sample

The population in this study are people who have used

BNI mobile banking . The sampling technique in this

study used a random sampling technique , namely a

sampling technique in which all individuals in the

population either individually or together are given

the same opportunity to be selected as sample

members.

In determining the sample, if the population is

large and the number is unknown, then according to

Widianto (2008:35) the formula is used:

H2: Service Innovation has a positive effect on E-

Satisfaction

n

𝑍

4 𝑀𝑜𝑒²

Information :

n = number of samples

Z = Z value with 95% confidence level

then the value of Z = 1.96 (distribution table

normal)

Moe = margin of error or maximum error

is 10%. By using a margin of error of 10%,

the minimum number of samples that can be

taken is:

n = 1.962 / 4 (0 .10 ) ²

n = 96 .04 which is rounded to 97

In order for this study to be more fit, in this study

a sample of 100 people was taken. The reason the

sample is rounded up to 100 people is because if one

E-Satisfaction

(Y)

ICOSOP 2022 - International Conference on Social and Political Development 4

386

of the questionnaires contains data that is not valid, it

can use the more filling in the questionnaire. The

number of respondents as many as 100 people is

considered representative because it is greater than

the minimum sample limit.

4 RESULTS AND DISCUSSION

4.1 Validity and Reliability Test

4.1.1 Validity Test

The validity test was carried out with the aim of

testing the validity of each question item on the

questionnaire that had been designed. A question

item is said to be valid if the correlation value (R h

count) of the question item > R table (0.361) . Table

4. 1 presents the results of the validity test for each

question item from the questionnaire.

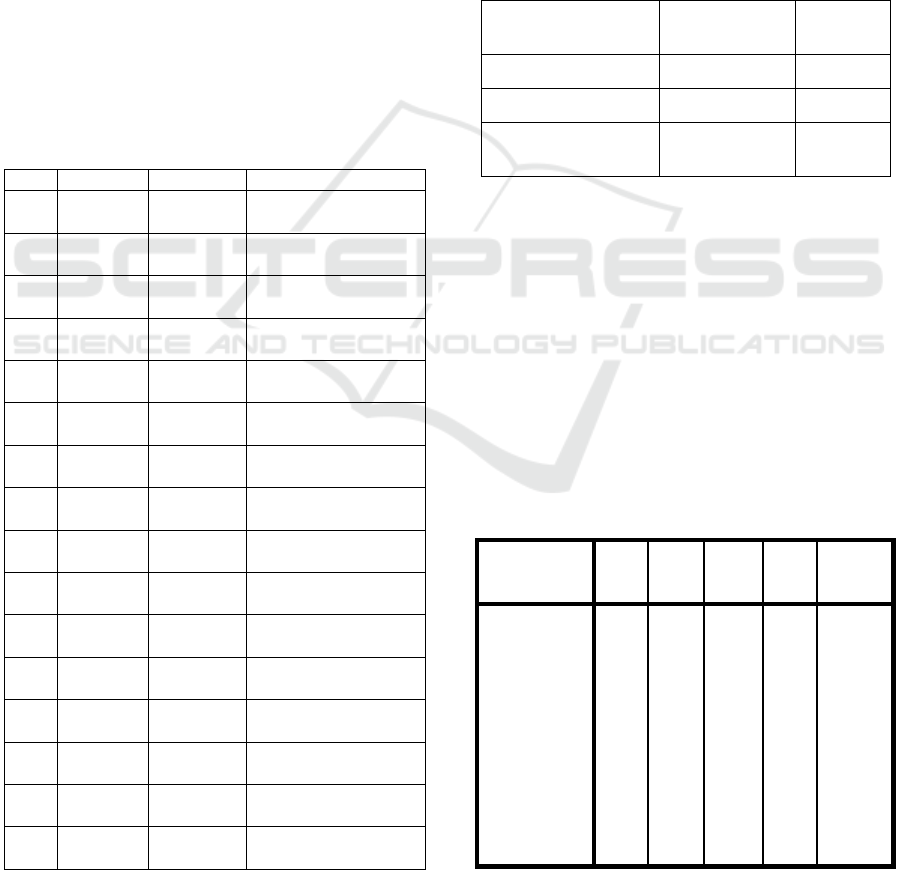

Table 4.1 Validity Test of Questionnaire Question Item

P R Count R Table Results

Y11 0.769 0.361

Valid (R Count > R

Table

)

Y12 0.618 0.361

Valid (R Count > R

Table)

Y13 0.78 0.361

Valid (R Count > R

Table)

Y14 0.863 0.361

Valid (R Count > R

Table

)

X11 0.815 0.361

Valid (R Count > R

Table

)

X12 0.877 0.361

Valid (R Count > R

Table)

X13 0.888 0.361

Valid (R Count > R

Table

)

X14 0.763 0.361

Valid (R Count > R

Table

)

X15 0.849 0.361

Valid (R Count > R

Table)

X16 0.877 0.361

Valid (R Count > R

Table)

X17 0.855 0.361

Valid (R Count > R

Table

)

X18 0.882 0.361

Valid (R Count > R

Table)

X21 0.762 0.361

Valid (R Count > R

Table)

X22 0.761 0.361

Valid (R Count > R

Table

)

X23 0.65 0.361

Valid (R Count > R

Table)

X24 0.804 0.361

Valid (R Count > R

Table)

A question is said to be valid if the value of R

count> 0.3 61 (R table ). It is known that all calculated

R values are > 0.3 61 (R table ). So it can be

concluded that all of the questionnaires are valid.

4.1.2 Reliability Test

Reliability testing must be done only on questions

that already have or meet the validity test, so if it

doesn't meet the validity test requirements then it

doesn't need to be continued for reliability testing .

The following are the results of the reliability test on

valid question items.

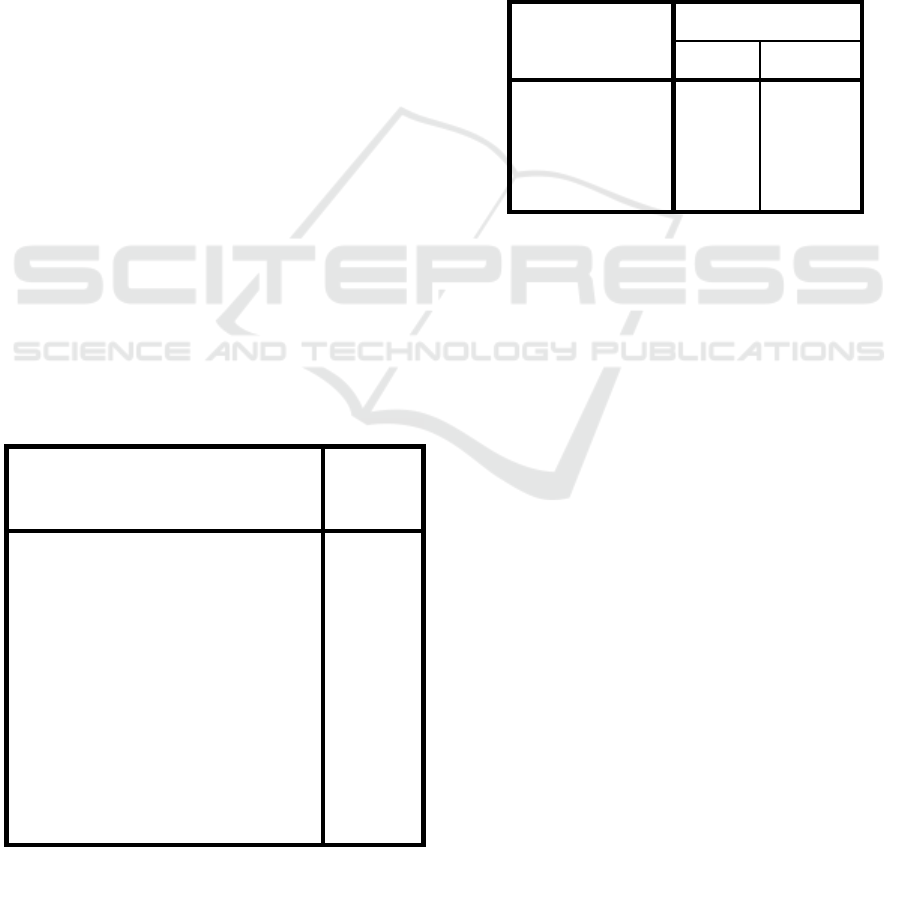

Table 4.2 Reliability Test

Variable

Cronbach's

Alpha Results

E-Satisfaction (Y) 0.882 Reliable

Self Service (X1) 0.959 Reliable

Service Innovation

(X2) 0.88 Reliable

If the value of Cronbach's Alpha greater than 0.6,

then the research questionnaire is reliable. It is known

that the questionnaire is reliable, because all values of

Cronbach's Alpha greater than 0.6.

4.2 Descriptive Statistical Analysis

In the descriptive analysis section, the minimum,

maximum, average and standard deviation values are

presented based on e-satisfaction, self service

technology and service innovation.

Table 4.3 Descriptive Statistics

Descri

p

tive Statistics

N

Minim

um

Maxim

um Mean

Std.

Deviation

E-Satisfaction

(Y)

100 2.75 4.75

3.807

5

.45762

Self Service

(X1)

100 1.38 5.00

3.730

0

.70526

M-

Payment(X2)

Innovation

100 1.25 5.00

3.595

0

.66646

Valid N

(listwise)

100

The Effect of Service Innovation and Self Service Technology on Customer Satisfaction PT Bank Negara Indonesia (Persero) Tbk Kc Medan

387

Based on Table 4.3 , it is known that the minimum

value of e-satisfaction is 2.75, while the maximum

value of e-satisfaction is 4.75. The average e-

satisfaction is 3.8075, with a standard deviation of

0.45762. It is known that the minimum value of self-

service is 1.38, while the maximum value of self-

service is 5. The average value of self-service is

3.7300, with a standard deviation 0.70526. It is

known that the minimum value of m-payment

innovation is 1.25, while the maximum value of m-

payment innovation is 5. The average value of m-

payment innovation is 3.5950, with a standard

deviation of 0.66646.

4.3 Classical Assumption Test

4.3.1 Normality Test

The normality test aims to test whether in the

regression model, the confounding or residual

variables have a normal distribution. Test tand

Fassume that the residual value follows a normal

distribution. In this study, the normality test of the

residuals using the Kolmogorov-Smirnov test. The

level of significance used is α=0,05. The basis for

making decisions is to look at the probability numbers

p, with the following conditions.

the probability value is p≥0.05, then the assumption

of normality is met.

If the probability < 0.05 then the assumption of

normality is not met.

Table 4.4 Normality Test

One-Sample Kolmogorov-Smirnov Test

Unstandard

ized

Residual

N 100

Normal Parameters

a,,b

mean .0000000

Std. Deviation .39233875

Most Extreme

Differences

Absolute .046

Positive .045

negative -.046

Kolmogorov-Smirnov Z .459

asymp. Sig. (2-tailed) .984

a. Test distribution is Normal.

b. Calculated from data.

Note that based on Table 4.4, the probability value

por Asymp is known. Sig. (2-tailed) of 0.984. Due to

the probability value p, which is 0.984, greater than

the level of significance, which is 0.05. This means

that the data is normally distributed 1.

4.3.2 Multicollinearity Test

To check whether there is multicollinearity or not, it

can be seen from the value of the variance inflation

factor (VIF). A VIF value that is more than 10

indicates that an independent variable has

multicollinearity (Ghozali, 2013).

Table 4.5 Multicollinearity Test

Model

Collinearity Statistics

Tolerance VIF

1 (Constant)

Self Service (X1) .998 1.002

Service

Innovation (X2)

.998 1.002

Note that based on Table 4.5, it is known that the

VIF value of self service technology is 1.002, while

the maximum value of service innovation is 1.002.

Because all VIF values < 10, it is concluded that there

is no multicollinearity.

4.3.3 Heteroscedasticity Test

Detection of the presence or absence of

heteroscedasticity can be done by looking at the

presence or absence of certain patterns on the scatter

plot graph between SRESID on the Y axis, and

ZPRED on the X axis ( Ghozali, 2013). Ghozali

(2013) states that the basis of the analysis is that if

there is a certain pattern, such as the points that form

a certain regular pattern, it indicates that

heteroscedasticity has occurred. If there is no clear

pattern, and the points spread above and below the

number 0 on the Y axis, then there is no

heteroscedasticity.

4.4 Hypothesis Test

4.4.1 Simultaneous Significance Test (F

Test)

The F test aims to test the effect of the independent

variables together or simultaneously on the dependent

variable e-satisfaction.

ICOSOP 2022 - International Conference on Social and Political Development 4

388

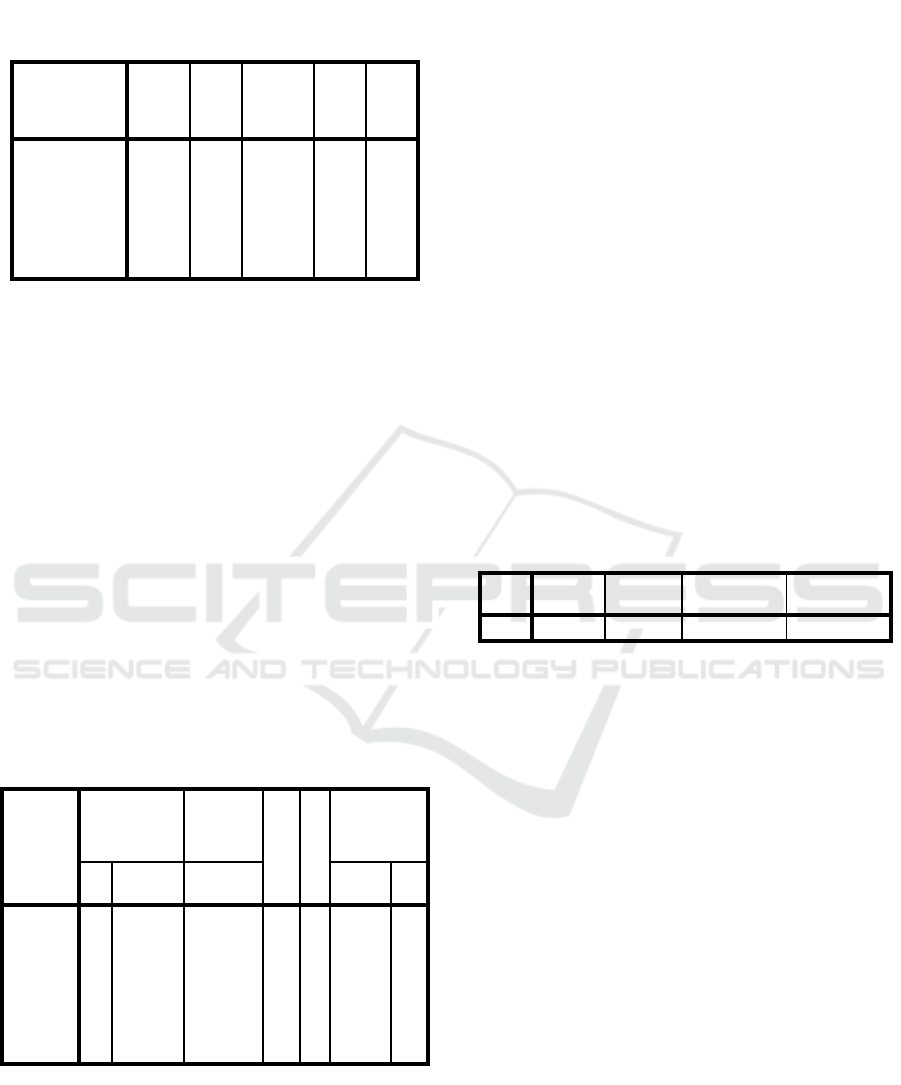

Table 4.6 Simultaneous Effect Test (F Test)

ANOVA

b

Model

Sum of

Square

s Df

Mean

Square F Sig.

1 Regressio

n

5.493 2 2,746 17,48

2

.000

a

Residual 15,239 97 .157

Total 20.732 99

a. Predictors: (Constant), Service Innovation(X2), Self Service

Technology (X1)

b

. Dependent Variable: E-Satisfaction (Y)

Based on Table 4.6, it is known that the calculated

F value is 18 .966 and the Sig value. is 0.000. It is

known that the calculated F value is 17 ,482 > F table

3 , 09 and the Sig value is 0.000 < 0, 05 , then self

service technology and service innovation together or

simultaneously have a significant effect on e-

satisfaction.

4.4.2 Test of Partial Significance (t Test)

Statistical t test was used to determine the level of

significance of the effect of each independent variable

on the dependent variable. Table 4.7 presents the

value of the regression coefficient, as well as the

value of the t statistic for partial effect testing.

Table 4.7 Test of Significance of Partial Influence (Test t)

Coefficients

a

Model

Unstandardized

Coefficients

Standardiz

ed

Coefficient

s

t

Sig

.

Collinearity

Statistics

B Std. Erro

r

Beta

Toleranc

e VIF

1 (Constan

t)

200

8

.311

6.45

9

.00

0

Self

Service

(X1)

.200 .057 .308 353

7

.00

1

.998 1.00

2

Service

Innovatio

n (X2)

.293 .060 .427 4.89

9

.00

0

.998 1.00

2

a. Dependent Variable: E-Satisfaction (Y)

Based on the results in Table 4.7, the following

regression equation is obtained.

Y = 2.008 + 0.200X1 + 0.293X2 + e

Based on the results in Table 4.7:

1. Self service technology has a positive effect

on e-satisfaction, with a regression

coefficient value of 0.200, and significant,

with a t-value = 3.537 > 1.98 and a Sig value.

= 0.001 < 0.05. So it can be concluded that

self service technology has a positive and

significant effect on e-satisfaction.

2. Service innovation has a positive effect on e-

satisfaction, with a regression coefficient

value of 0.293, and is significant, with a t-

count value = 4.899 > 1.98 and a Sig value.

= 0.000 < 0.05. So it can be concluded that

service innovation has a positive and

significant effect on e-satisfaction.

4.4.3 Analysis of the Coefficient of

Determination

The coefficient of determination (R

2

) is a value (the

value of the proportion) that measures how much the

ability of the independent variables used in the

regression equation to explain the variation of the

dependent variable.

Table 4.8 Coefficient of Determination

Model Summary

b

Model R R Square

Adjusted R

Square

Std. Error of

the Estimate

1 .515

a

.265 .250 .39636

a. Predictors: (Constant), Service Innovation(X2), Self Service

Technology(X1)

b. Dependent Variable: E-Satisfaction (Y)

Based on Table 4.8, it is known that the

coefficient of determination (R-Square ) is 0.265.

This value can be interpreted that the variable of self

service technology and service innovation is able to

influence e-satisfaction by 26.5 % , the remaining

100% - 26.5 % = 73.5% is explained by other

variables or factors.

5 CONCLUSIONS

Based on the results of the study, it can be concluded

that:

1. Self service technology and service innovation

are able to influence e-satisfaction by 26.5% ,

the remaining 100% - 26.5 % = 73.5% is

explained by other variables or factors.

2. Self service technology and service innovation

together or simultaneously have a significant

effect on e-satisfaction.

The Effect of Service Innovation and Self Service Technology on Customer Satisfaction PT Bank Negara Indonesia (Persero) Tbk Kc Medan

389

3. Self service technology has a positive effect on

e-satisfaction , with a regression coefficient

value of 0.200, and significant, with a t-count

value = 3.537 > 1.98 and a Sig value. = 0.001 <

0.05. So it can be concluded that self service

technology has a positive and significant effect

on e-satisfaction.

4. Service innovation has a positive effect on e-

satisfaction , with a regression coefficient value

of 0.293, and is significant, with a t-count value

= 4.899 > 1.98 and a Sig value. = 0.000 < 0.05.

So it can be concluded that service innovation

has a positive and significant effect on e-

satisfaction.

REFERENCES

Delafrooz , nNarges et al. (2013). The Impact Of Service

Innovation On Consumer Satisfaction . 3 (2).Smith, J.,

1998. The book, The publishing company. London, 2

nd

edition.

Demirici, Orel & Kara, Ali. (2013). Supermarket Self

Checkout Service Quality, Customer Satisfaction, and

Loyalty: Empirical Evidence from an Emerging

Market. Journal of Retailing and Consumer

Service.Smith, J., 1998. The book, The publishing

company. London, 2

nd

edition.

D en Hertog, P. , van der Aa , W. and de Jong, MW (2010),

"Capabilities for managing service innovation: towards

a conceptual framework", Journal of Service

Management , Vol. 21 No. 4, pp. 490-514.Smith, J.,

1998. The book, The publishing company. London, 2

nd

edition.

Drucker, PF (2012). Innovation and Entrepreneurship .

Jakarta: Erlangga.

Evan Setiawan (2016) “The Effect of Failure and Self

Service Technology Recovery on Online Shopping

Experience, Satisfaction and Repurchase Intention: An

Overview from a Critical Sdl Perspective” Baabu Al-

Ilmi Vol. 1 No.2Smith, J., 1998. The book, The

publishing company. London, 2

nd

edition.

Fandy, Tjiptono. 2011. Service Management Realizing

Excellent Service . Edition 2. Yogyakarta: Andi.Smith,

J., 1998. The book, The publishing company. London,

2

nd

edition.

Fandi, Tjiptono. 2014. Service, Quality & Satisfaction.

Edition 3. Yogyakarta: Andi Publisher.Smith, J., 1998.

The book, The publishing company. London, 2

nd

edition.

Ghozali, Imam. 2013. Application of Multivariate Analysis

with IBM SPSS 21 Update PLS Regression Program.

Semarang: Diponegoro University Publishing Agency.

Kotler and Keller. 2009. Marketing Management . Volume

I. 13th Edition. Jakarta: Erlangga

Lin, JC and Hsieh, P. (2006), "The role of technology

readiness in customers' perception and adoption of self-

service technologies", International Journal of Service

Industry Management , Vol. 17 No. 5, pp. 497-517

Lovelock, Christopher, et al. 2012. Marketing Services.

Volume I Seventh Edition. Translation by Dian

Wulandari & Devri Barnadi Putera. 2010. Jakarta:

Erlangga

McCollough, M.A , Berry. LL, & Yadav, MS An empirical

investigation or customer satisfaction after service

failure and recovery. Journal of service research , 3(2),

2000.p.121- I 37Smith, J., 1998. The book, The

publishing company. London, 2

nd

edition.

Meuter, ML, Ostrom, AL, Roundtree, RI, & Bitner, MJ

(2000). Self-service Technologies: Understanding

Customer Satisfaction with Technology-Based Service

Encounters. Journal of Marketing, 64(3), 50–64.

Oliver, Riscrd L, (1997), Satisfaction A Behavioral

Perspective On The Consumer. McGraw-Hill

Education, Singapore.

Rew, D. , Jung, J. and Lovett, S. (2021), "Examining the

relationships between innovation, quality, productivity,

and customer satisfaction in pure service companies",

The TQM Journal , Vol. 33 No. 1, pp. 57-70.

Sakun Boon-itt, (2015) "Managing self-service technology

service quality to enhance e-satisfaction", International

Journal of Quality and Service Sciences, Vol. 7 Issue:

4, pp.373-391

Simon, A. and Honore Petnji Yaya, L. (2012), "Improving

innovation and customer satisfaction through systems

integration", Industrial Management & Data Systems ,

Vol. 112 No. 7, pp. 1026-1043.

ICOSOP 2022 - International Conference on Social and Political Development 4

390