Research on the Application of Blockchain Technology in the

Innovative Development of Agricultural Supply Chain Finance

Chunhua Li

Xi'an eurasia university, China

Keywords: Blockchain, Supply Chain Finance, Distribution of Benefits, "Agriculture, Rural Areas and Farmers".

Abstract: Supply chain finance can provide high-quality financing channels for agriculture, rural areas and farmers to

support the development of agricultural industry chain, but agricultural supply chain finance has not reached

the maturity in the industrial field, the agricultural supply chain structure is loose, the enterprise

qualification is quite different, the agricultural industry itself has a special attribute determines the

agricultural and industrial supply chain finance innovation mechanism is significantly different. This paper

analyzes the construction method of embedding the key technology of blockchain into agricultural supply

chain finance to solve the problems of "difficult financing, expensive financing and slow financing" of

agriculture-related smes from the technical level. Combined with the characteristics of agricultural

cooperatives, a "1+1+N" supply chain finance architecture was proposed to solve the problem of loose

structure of agricultural supply chain from the management level, and the agricultural supply chain finance

model was innovated on a sub-basis by combining blockchain technology. Shapley value method was used

to construct the financial benefit distribution model of agricultural supply chain, and the incentive

mechanism of participating enterprises in supply chain finance was discussed by means of the benefit

distribution model. The research results enrich the application of blockchain in the fields related to

agricultural supply chain finance, and contribute to the establishment of supply chain financing environment

for small, medium and micro agriculture-related enterprises based on cooperatives, thus contributing to rural

revitalization.

1 INTRODUCTION

According to the data from the Blue Book of Internet

Finance for "Agriculture, Countryside and Farmers"

released by the Chinese Academy of Social Sciences,

the financial gap for "agriculture, countryside and

farmers" in China has reached 3.05 trillion yuan, and

there is still much room for improvement in the

revitalization of financial services for rural industries.

At present, China's rural financial resources are

seriously deficient. The systems of rural homestead

mortgage, agricultural product mortgage, rural land

contractual management right mortgage, and

agricultural product insurance are not perfect. Small,

medium-sized and micro agricultural enterprises and

farmers have limited financing channels, large

financing difficulties, long financing cycle, and high

financing costs. These problems are closely related to

the existing supply chain status of agricultural

enterprises.

2 LITERATURE REVIEW

Ahluwalia Saurabh et al. (2020) analyzed how to use

blockchain technology for start-up financing, and

proposed a model based on the theory of transaction

cost economics and the transaction nature of

blockchain technology to demonstrate how to use

blockchain technology to overcome many problems

inherent in start-up financing of enterprises

(Ahluwalia, 2020). Feng Bao et al. (2022) takes the

platform-type supply chain finance financing

business as the research object, analyzes the factors

that affect the decision-making of participants, builds

a tripartitic evolutionary game model of smes, core

enterprises and financial institutions under traditional

circumstances and under the drive of blockchain,

respectively, and explores the balanced choice of

each participant (Feng, 2022). Huo Hong et al.

(2022) aiming at the agricultural supply chain

composed of e-commerce, farmers and leading

enterprises, took into account the bankruptcy risk of

Li, C.

Research on the Application of Blockchain Technology in the Innovative Development of Agricultural Supply Chain Finance.

DOI: 10.5220/0012036300003620

In Proceedings of the 4th International Conference on Economic Management and Model Engineering (ICEMME 2022), pages 529-534

ISBN: 978-989-758-636-1

Copyright

c

2023 by SCITEPRESS – Science and Technology Publications, Lda. Under CC license (CC BY-NC-ND 4.0)

529

farmers and the output randomness of agricultural

products, respectively built the income model of

e-commerce, farmers and leading enterprises under

the insurance and risk sharing mode, and proposed

the optimal decision of e-commerce, farmers and

leading enterprises and the influencing factors of the

optimal decision (Huo, 2022). Sun Zhonghe and Xu

Xiaoyan et al. (2021) selected 11 risk assessment

indicators of agricultural supply chain finance

business, built an agricultural supply chain risk

assessment model based on GA-BP neural network,

and verified the proposed risk assessment model with

case analysis (Sun, 2021). Wang Y. (2021) Combined

blockchain and fuzzy neural network algorithm,

studied the credit risk of SME financing from the

perspective of SME financing, built the supply chain

financial information module by integrating the

financial system with blockchain technology, adopted

fuzzy neural network algorithm for financial data

processing and risk assessment, and effectively

solved and improved the risk handling level of

financial enterprises (Wang, 2021). Based on the

current development status of agricultural supply

chain finance in China, Zheng Yi (2022) analyzed the

main models and development difficulties of supply

chain finance and proposed innovative strategies of

agricultural supply chain finance (Zheng, 2022).

To sum up, domestic and foreign scholars'

research on supply chain finance has combined

financial technologies such as blockchain, and some

literatures have studied the profit distribution and

balanced selection of various participants in supply

chain finance. It rarely discusses the promotion and

promotion of the internal drive of the agricultural

supply chain financial model in combination with the

characteristics of the agricultural supply chain. This

paper uses the research experience of domestic and

foreign scholars for reference, relies on the

agricultural supply chain financial model innovation

and benefit distribution model, solves the problems

of loose and difficult management of the agricultural

supply chain structure, and relies on the blockchain

technology to solve the key problems in the

implementation of supply chain finance.

3 METHODS AND ANALYSIS

3.1 Analysis of Key Issues in the

Implementation of Agricultural

Supply Chain Finance

First, Cause analysis of financing difficulties. The

supply chain finance relies on the core enterprise's

ability to control goods and adjust sales. For the sake

of risk control, the capital end is generally willing to

provide financial services only to the core enterprise's

upstream and downstream primary suppliers and

dealers, which leads to the failure to meet the needs of

secondary and tertiary suppliers/dealers with huge

financing needs. In addition, bills cannot be separated

during the financing process, and the flexibility of use

is very limited. Therefore, the main problems in

financing are credit multi-level transmission, bill

splitting and trust consensus.

Second, the characteristics of supply chain

finance require participants to have a very detailed

and full understanding of the whole industry chain,

and have high requirements on the control ability and

technical ability of underlying assets. In order to

reduce risks, it is difficult to reduce the operating

costs of supply chain finance. In addition, the supply

chain financing business lacks a regulatory body in

the implementation process. In order to obtain

financing, SMEs make unlimited concessions in the

discount rate, which makes the overall financing cost

of the supply chain rise. Therefore, the problem of

expensive financing mainly lies in the consensus of

trust, the achievement of risk management and

control, and the cooperation of enterprises in the

agricultural supply chain.

Third, agriculture itself has a long production

input cycle, and there is a serious problem of

information islands in the agricultural supply chain

system. Pledged goods are stored in third-party

logistics companies, and it is difficult to verify the

authenticity, quality, status, transaction and other

storage information of goods, which increases the

difficulty of information audit and lengthens the audit

cycle. Therefore, the problem of slow financing is

mainly the difficulty of preventing bill fraud and the

achievement of the efficiency of bill information

review.

Therefore, the key issues of agricultural supply

chain financial development can be summarized as

trust consensus, bill splitting, credit transmission, risk

control, bill cost, slow information review, etc.

3.2 Construction Method of New

Model of Agricultural Supply

Chain Finance Implanted with

Blockchain Technology

3.2.1 Construction of Agricultural Supply

Chain Financial Data System

Based on blockchain and big data technology, build a

ICEMME 2022 - The International Conference on Economic Management and Model Engineering

530

visual, tamper proof, non replicable and traceable

agricultural supply chain financial data platform, and

rely on this platform to achieve online data storage

and business online operation on the agricultural

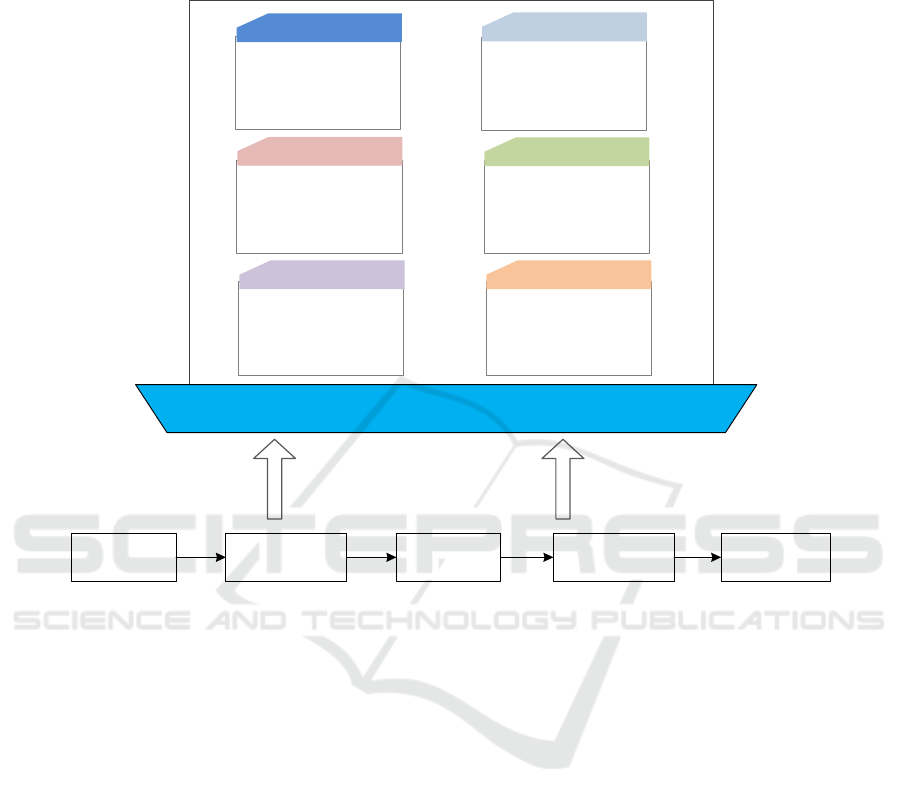

supply chain., as shown in Figure 1.

Core

Enterprise

Downstream

enterprises

Upstream

enterprise

On-chain

data store

On-chain

business operations

Data read, data write,

data authorization, time

stamp

Logistics, information

flow, capital flow,

business flow data

storage, financing data

storage

Encryption of trade

information and supply

chain financing

information

Voucher split, voucher

transfer, voucher

financing

Contract online

automatic execution,

voucher automatic

review, automatic

lending, automatic

repayment

Record the transaction

information of each link

of enterprises and

implement the right

confirmation

Agricultural supply chain finance platform

Block management

Smart contract

Distributed data

storage

certificate

consensus

Encryption of

information

Third party

logistics

Third party

logistics

Figure 1: Core module of agricultural supply chain finance platform

Suppliers, core enterprises, distributors, retailers,

third-party logistics companies, banks and other

financial institutions in the supply chain create

blockchain users. Block users record logistics, capital

flow, information flow, business flow and other

information related to their own business, and upload

them to the agricultural supply chain financial

platform. These data are recorded synchronously in

each enterprise with the occurrence of business in the

supply chain, A decentralized database of the whole

supply chain process has been formed. Of course, it is

not safe to disclose all these information. Therefore,

the asymmetric encryption algorithm is used to

encrypt the data uploaded by enterprises with public

keys, and different users are given different download

permissions. When enterprises download the data

they need, they use the private key to decrypt it.

3.2.2 Implementation Logic of Trust

Consensus

Under the blockchain framework, the upstream and

downstream enterprises and financial institutions of

the supply chain, as node enterprises, can obtain

system data at any time. The decentralized distributed

structure can solve the problem of information

asymmetry. Node enterprises do not need to trust a

single node in a centralized way, and also save a lot of

intermediate costs. In addition, due to the tamper

proof, non replicable and traceability of blockchain

technology, the reliability of transaction information

has been improved, thus establishing the trust

consensus of all participants in the supply chain.

3.2.3 Implementation Logic of Bill and

Transaction Information Fraud

Prevention

The ledger distribution feature of the blockchain

enables the supply chain system to automatically

form data that cannot be tampered with, and these

data will be confirmed in real time by the blockchain

technology, which not only reduces the delay, but also

solves the problem of information audit. The tamper

proof timestamp can solve the problem of data

tracking and information anti-counterfeiting. In

Research on the Application of Blockchain Technology in the Innovative Development of Agricultural Supply Chain Finance

531

addition, the data blocks in the blockchain are

connected in order and form an tamper proof data

chain. Timestamps attach a set of real data that cannot

be forged to all transactions, which can effectively

prevent bill forgery, information distortion and other

problems.

3.2.4 Information Audit Efficiency

Improvement

Since the system stores reliable and tamper proof

data, as a computer execution language, smart

contracts can eliminate all artificial obstacles to the

execution of the contract and realize the automatic

transfer of capital, goods, claims and other assets

under the condition that the set conditions are met. It

is mandatory and solves the problem of low

efficiency and high cost of labor.

3.2.5 Implementation Logic of Credit

Transfer and Bill Disassembly

Under the traditional supply chain finance mode, only

enterprises with direct transaction relationship with

core enterprises can be supported to finance. The

credit of core enterprises cannot be transferred, and

the accounts receivable vouchers cannot be

disassembled. Under the blockchain structure, the

token disassembles the credit of the detachable core

enterprises and transfers the credit level by level, so

that the upstream and downstream remote enterprises

of the supply chain can enjoy the credit guarantee of

the core enterprises, expand the financial benefit

coverage of the supply chain, and meet the financing

needs of all SMEs in the supply chain.

3.3 Basic Principle of “Shapley” Value

Method

In the supply chain finance business, core enterprises,

agriculture-related smes and financial institutions

form an alliance to pursue the effect of 1+1>2. The

prerequisite for the long-term, sustainable and stable

cooperation of such an alliance is that all parties can

obtain their due share of income in the income

distribution. In this paper, the benefits of alliance

members are distributed based on the "Shapley"

value method, which can reflect the contribution

degree of each participating enterprise to the overall

goal of supply chain finance, and has good rationality

and fairness. Specific assumptions are as follows:

Let I be the enterprise set of the cooperative

alliance of n participants, expressed as I:{1,2... , n},

participants set S is a subset of the I (S ⊆ I), expressed

in V (S) each of the participants set S corresponding

revenue function, meet:

()

()()()

ISSSSSVSVSSV

V

⊆=∩+≥∪

=

21212121

,,,

0

φ

φ

(1)

Formula (1) indicates that the revenue of any two

disjoint enterprise sets in the case of cooperation is no

less than the revenue of non-cooperation. Therefore,

when all the participants cooperate, the maximum

revenue will be reached, which is denoted as V(I).At

this time, X

i

is used to represent the income

distribution quota obtained by members i of the

largest aggregate I from the maximum cooperation

income V(I) according to their contribution degree,

forming an n-dimensional vector X=(X

1

, X

2

,..., X

n

),

which meets the following conditions:

(1) Meet the individual rationality, that is, the

income of an enterprise when it joins the alliance and

chooses to cooperate must not be less than the income

of its own independent operation, otherwise the

enterprise will not choose to join, so X

i

≥ V (i).

(2) Meet the overall rational condition, that is, the

total income obtained by the alliance must be fully

distributed, otherwise all member enterprises will not

agree to this distribution scheme, so

n

I

VX

,...,2,1i,

n

1i

i

=

=

=

According to the "Shapley" value method, the

income distribution amount X

i

of participating

enterprise i is called the "Shapley" value, which is

recorded as φ

i

(E). The calculation formula is as

follows:

()

()

() ()

[]

()

!

其中

n

1)!-()!-(n

i

SS

SW

ISVSVSWE

IS

=

−=

⊆

ϕ

(2)

N is the number of all participants in set I, |s| is the

number of cooperative enterprises in subset S, V(S) is

the overall income of subset S, V (S/I) is the income

obtained when member i does not participate in

cooperation in subset S, and W(|s|) is the weighting

factor.

4 RESULTS

4.1 "1+1+N" Financial Model of

Agricultural Supply Chain

The "1+1+N" agricultural supply chain financial

model is a new agricultural supply chain financial

model operated by one leading enterprise and one

ICEMME 2022 - The International Conference on Economic Management and Model Engineering

532

rural cooperative. N refers to small and medium-sized

agricultural enterprises, logistics companies,

commercial banks, etc. Leading enterprises have

market influence and good qualifications, which are

suitable for endorsing all links of supply chain

financing, and can play a leading and promoting role

in the development of supply chain finance; As a

special organization, the cooperative has a deep

foundation of farmers and financial support from the

state. It has natural advantages in the collection of

supply chain financial data. Therefore, the rural

cooperative is most suitable for the operation of the

agricultural supply chain financial data platform, and

is responsible for the specific business of the supply

chain financial data platform, such as platform

building, daily operation, data maintenance, etc. The

agricultural supply chain financial platform operated

by cooperatives has the objectivity and timeliness of

information. The addition of blockchain technology

makes the data tamper proof and open, and enables

the bill to be disassembled and the transaction

efficiency to be improved. In this way, an open

platform jointly recognized by enterprises has been

formed. All small and medium-sized agricultural

enterprises, financial institutions and logistics

companies that are interested in participating in the

supply chain financial business can register on the

platform, Participate in it and make profits

respectively. This mode is applicable to most types of

agricultural supply chains, and the overall

architecture is shown in Figure 2.

Rural cooperatives

Small and medium-sized

agricultural enterprises,

logistics companies,

commercial banks, etc

1

Leading

enterprise

1 N

Figure 2: Financial structure of agricultural supply chain.

4.2 Construction of Financial Benefit

Distribution Model in Agricultural

Supply Chain

The existence of rural cooperatives is to improve the

level of farmers' organization, promote the

development of agricultural production and increase

farmers' income. It is an important window for

farmers to talk with the government. The primary

purpose of the establishment of cooperatives is not to

earn excess profits, and there are national financial

subsidies. From the perspective of model

construction, cooperatives maintain the platform and

do not directly create benefits for the supply chain

alliance. According to the nominal representative

axiom of the "Shaley" value method, those who have

not made contributions to the system should not share

the benefits, which is called nominal representatives.

Therefore, in combination with the "1+1+N"

agricultural supply chain financial model, the interest

distribution among financing enterprises (i.e.

agricultural SMEs), commercial banks and leading

enterprises is mainly considered.

Suppose the financing enterprise is X, the

commercial bank is Y, and the leading enterprise is Z,

then I={X, Y, Z}, the cooperation between X and Y is

XY, the cooperation between X and Z is XZ, the

cooperation between Y and Z is YZ, and the supply

chain alliance formed by X, Y, and Z is XYZ. Set the

annual profits of financing enterprises, commercial

banks and leading enterprises when they operate

alone and do not participate in cooperation as x, y and

z respectively, and the expected income of X and Y

cooperation is a; the expected income of X and Z

cooperation is b; the expected income of Y and Z

cooperation is c. If X Y and Z cooperate to form a

supply chain alliance, and the expected income is d.

According to formula (2), calculate the benefit

distribution table of each participating enterprise, as

shown in Table 1:

Table 1: φ

i

(E) value solution table

S

X

V(S) V(S/X) V(S)-V(S/X)

X x 0 x 1/3 x/3

XY a y a-y 1/6 (a-y)/6

XZ b z b-z 1/6 (b-z)/6

XYZ d c d-c 1/3 (d-c)/3

()

SW

()

() ()

[]

ISVSVSW −

Research on the Application of Blockchain Technology in the Innovative Development of Agricultural Supply Chain Finance

533

Therefore, the profit distribution of financing

enterprise X is:

()

()

() ()

[]

6/)d2cba2z2yx(

3/cd6/zb6/yax/3

i

+++−+−−=

−+−+−+=

−=

⊆

)()()(

ISVSVSWE

IS

ϕ

Similarly, the profit distribution of commercial

banks is (- x+2y-z+a-2b+c+2d)/6, and that of leading

enterprises is (- x-y+2z-2a+b+c+2d)/6.

5 DISCUSSION

When studying the benefits of each participant in the

supply chain, the "Shapley" value method mainly

distributes the total benefits of the supply chain

according to the contribution of each participant to

the supply chain. In the actual supply chain financial

business, according to the different risks undertaken

by the participating enterprises, on the basis of the

benefit distribution model, the participating

enterprises with large risks can allocate relatively

more benefits, so as to urge the supply chain related

enterprises to actively participate in the supply chain

financial business. In future research, risk correction

factors can be introduced to modify the Shapley

value, thus forming an improved supply chain

financial benefit allocation model.

6 CONCLUSIONS

This research enriches the relevant theories of

blockchain enabled supply chain finance. Through

the application of blockchain, the risk of "1+1+N"

agricultural supply chain financial model has been

greatly reduced. From the perspective of commercial

banks, the problems of trust consensus, risk

management and control, and bill cost of all

participating enterprises have been well solved; For

financing enterprises, problems such as bill splitting,

credit transmission and slow information review have

been solved; For leading enterprises, while helping

SMEs solve the capital problem, it has improved the

management and control ability of the agricultural

supply chain and the stickiness between enterprises,

thus boosting the development of the agricultural

industry chain.

FUNDING

This research is funded by the university level

scientific research of Xi'an Eurasian University

(Project No.: 2022XCZX04)

REFERENCES

Ahluwalia Saurabh, Mahto Raj V, Guerrero Maribel.

Blockchain technology and startup financing: A

transaction cost economics perspective[J].

Technological Forecasting and Social

Change,2020,151(2):119854~119863

Feng Bao, Zhang Zuo Minyang. Blockchain empowerment

and financial optimization of platform based supply

chain - game analysis based on cost perspective [J].

Journal of Chongqing University of Technology (Social

Sciences), 2022,36 (10): 110-121

Huo Hong, Jia Xuelian, Jiang Man, Xu Lingling. Research

on Decision making of Agricultural Product Supply

Chain under Different Risk Prevention Modes [J].

Computer Application and Software, 2022,39 (02):

68-74

Sun Zhongye, Xu Xiaoyan. Research on Financial Risk

Assessment of Agricultural Supply Chain -- Based on

GA-BP Neural Network Model [J]. Technical Economy

and Management Research, 2021 (08): 78-82

Wang Y. Research on supply chain financial risk

assessment based on blockchain and fuzzy neural

networks[J]. Wireless Communications and Mobile

Computing, 2021(2021)124~128

Zheng Yi. Innovative Development of Agricultural Supply

Chain Finance in the Transformation of Rural

Production Mode [J]. Agricultural Economy, 2022

(01): 115-117

ICEMME 2022 - The International Conference on Economic Management and Model Engineering

534